ffdcea689ff25928868bb573944c9503.ppt

- Количество слайдов: 69

Chapter 10

Managing Costs

Management by Exception

Setting Standards

Participation in Setting Standards

Perfection versus Practical Standards: A Behavioral Issue

Perfection versus Practical Standards: A Behavioral Issue

Use of Standards by Service Organizations

Cost Variance Analysis

A General Model for Variance Analysis

A General Model for Variance Analysis

A General Model for Variance Analysis

Standard Costs

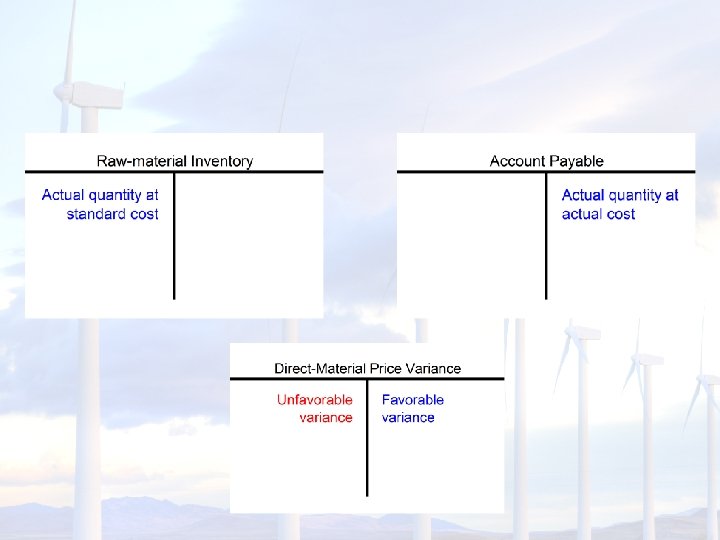

Material Variances

Material Variances

Material Variances

Material Variances

Material Variances

Material Variances

Material Variances

Material Variances

Material Variances

Material Variances Summary

Material Variances

Material Variances

Material Variances

Material Variances

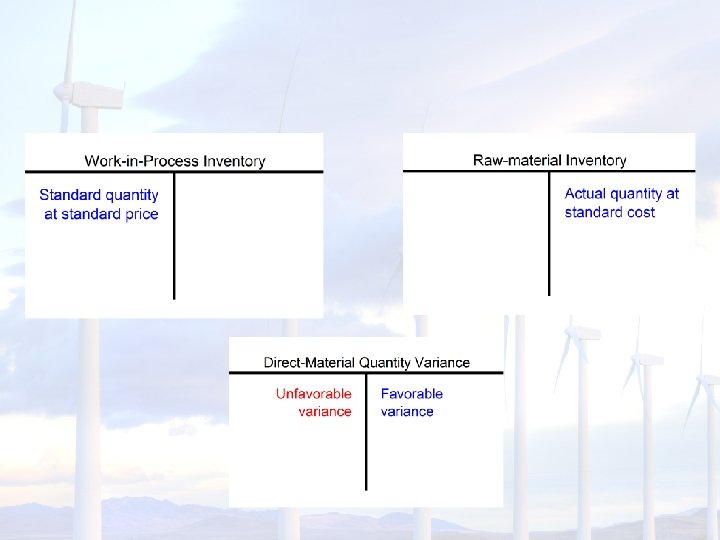

Isolation of Material Variances

Standard Costs

Labor Variances

Labor Variances

Labor Variances

Labor Variances

Labor Variances

Labor Variances

Labor Variances

Labor Variances

Labor Variances

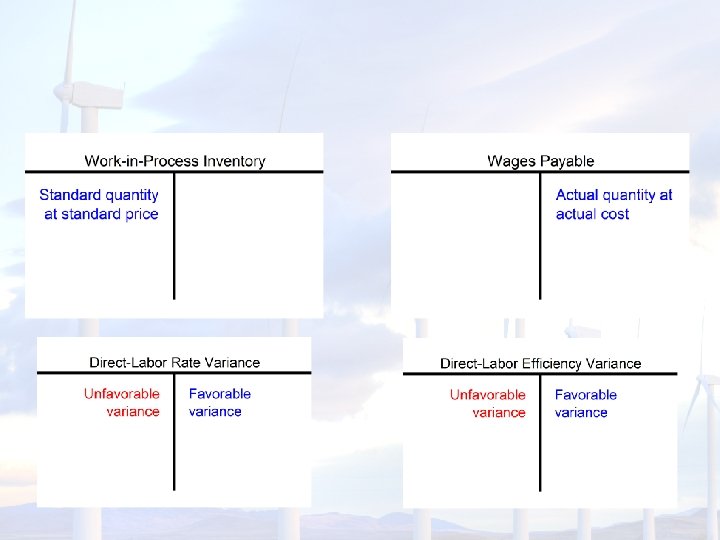

Labor Variances Summary

Significance of Cost Variances

Statistical Control Chart

Behavioral Impact of Standard Costing

Controllability of Variances

Interaction among Variances

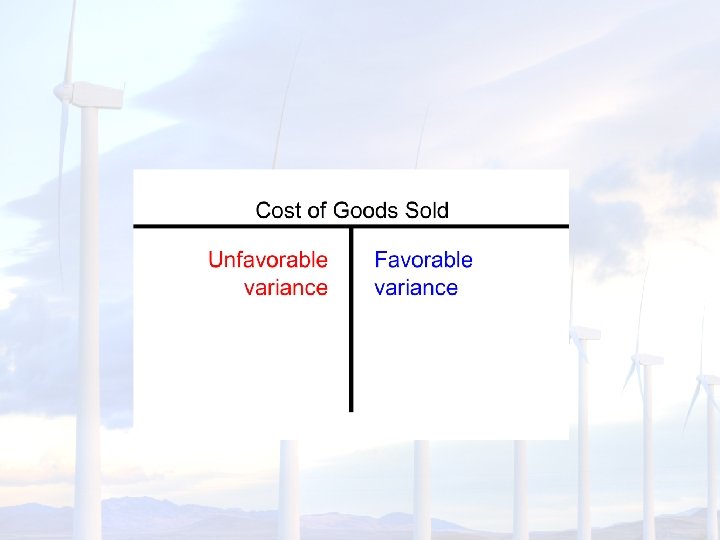

Standard Costs and Product Costing Standard material and labor costs are entered into Work-in-Process inventory instead of actual costs. Standard cost variances are closed directly to Cost of Goods Sold.

Advantages of Standard Costing

Criticisms of Standard Costing

The Balanced Scorecard

End of Chapter 10

ffdcea689ff25928868bb573944c9503.ppt