2d5e55f008f092bf2c64e91e39e71a48.ppt

- Количество слайдов: 50

CHANGES FOR 2009

CHANGES FOR 2009

Exemptions

Exemptions

Standard mileage rates have been changed for 2009: Business-related mileage: For 2009, the standard mileage rate for the cost of operating a car, van, or pickup/panel truck for business use is 55 cents per mile. Medical and move-related mileage: For 2009, the standard mileage rate for the cost of operating a vehicle for medical reasons or as part of a deductible move is 24 cents per mile. Charitable-related mileage: For 2009, the standard mileage rate for the cost of operating a vehicle for charitable purposes remains at 14 cents per mile.

Standard mileage rates have been changed for 2009: Business-related mileage: For 2009, the standard mileage rate for the cost of operating a car, van, or pickup/panel truck for business use is 55 cents per mile. Medical and move-related mileage: For 2009, the standard mileage rate for the cost of operating a vehicle for medical reasons or as part of a deductible move is 24 cents per mile. Charitable-related mileage: For 2009, the standard mileage rate for the cost of operating a vehicle for charitable purposes remains at 14 cents per mile.

New Vehicle Purchase

New Vehicle Purchase

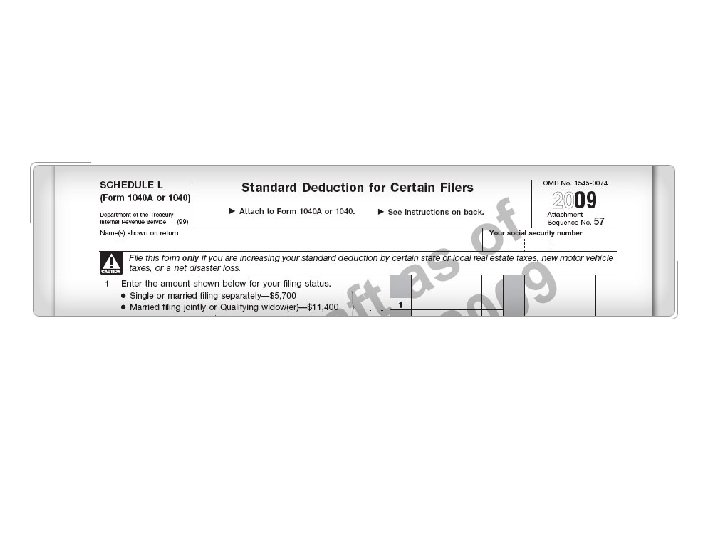

New Vehicle Purchase The deduction is limited to eligible taxes and fees paid on the first $49, 500 of the purchase price on the vehicle. The deduction phases out for taxpayers with modified AGI of more than $125, 000 ($250, 000 if Married Filing Jointly). The new vehicle deduction is available to taxpayers who claim the standard deduction, as well as taxpayers who itemize deductions on Schedule A (Form 1040). The new deduction can be used to increase the amount of the standard deduction or it can be taken as an itemized deduction (if the taxpayer is not electing to take the state and local general sales tax deduction).

New Vehicle Purchase The deduction is limited to eligible taxes and fees paid on the first $49, 500 of the purchase price on the vehicle. The deduction phases out for taxpayers with modified AGI of more than $125, 000 ($250, 000 if Married Filing Jointly). The new vehicle deduction is available to taxpayers who claim the standard deduction, as well as taxpayers who itemize deductions on Schedule A (Form 1040). The new deduction can be used to increase the amount of the standard deduction or it can be taken as an itemized deduction (if the taxpayer is not electing to take the state and local general sales tax deduction).

New Vehicle Purchase

New Vehicle Purchase

New Vehicle Purchase

New Vehicle Purchase

The maximum amount of the credit is increased to $2, 500 per student. In addition, 40 percent of the credit may be refundable. The credit is phased out for taxpayers with a modified AGI between $80, 000 and $90, 000 ($160, 000 and $180, 000 if Married Filing Jointly). Tip There are some exceptions for taxpayers claiming the Hope credit for a student who attended a school in a Midwestern disaster area in 2009. For more information, see Publication 4492 -B, Information for Affected Taxpayers in the Midwestern Disaster Areas, and Publication 970, Tax Benefits for Education.

The maximum amount of the credit is increased to $2, 500 per student. In addition, 40 percent of the credit may be refundable. The credit is phased out for taxpayers with a modified AGI between $80, 000 and $90, 000 ($160, 000 and $180, 000 if Married Filing Jointly). Tip There are some exceptions for taxpayers claiming the Hope credit for a student who attended a school in a Midwestern disaster area in 2009. For more information, see Publication 4492 -B, Information for Affected Taxpayers in the Midwestern Disaster Areas, and Publication 970, Tax Benefits for Education.

For 2009, the amount of the interest exclusion is phased out for Married Filing Jointly taxpayers or Qualifying Widow(er) taxpayers whose modified AGI is between $104, 900 and $134, 900. If the modified AGI is $134, 900 or more, no deduction is allowed. These are increased modified AGI amounts. Caution Married taxpayers who file separately do not qualify for the exclusion. For Single and Head of Household filing statuses, the interest exclusion is phased out for taxpayers whose modified AGI is between $69, 950 and $84, 950. If the modified AGI is $84, 950 or more, no deduction is allowed.

For 2009, the amount of the interest exclusion is phased out for Married Filing Jointly taxpayers or Qualifying Widow(er) taxpayers whose modified AGI is between $104, 900 and $134, 900. If the modified AGI is $134, 900 or more, no deduction is allowed. These are increased modified AGI amounts. Caution Married taxpayers who file separately do not qualify for the exclusion. For Single and Head of Household filing statuses, the interest exclusion is phased out for taxpayers whose modified AGI is between $69, 950 and $84, 950. If the modified AGI is $84, 950 or more, no deduction is allowed.

Definition of Qualifying Child

Definition of Qualifying Child

Definition of Qualifying Child

Definition of Qualifying Child

Additional Child Tax Credit

Additional Child Tax Credit

For tax years beginning after July 2, 2008 (the 2009 calendar year for most taxpayers), new rules apply to allow the custodial parent to revoke a release of claim to exemption that was previously released to the noncustodial parent on Form 8332, Release/Revocation of Release of Claim to Exemption for Child by Custodial Parent, or similar form. The revocation is effective no earlier than the tax year beginning in the calendar year following the calendar year in which the custodial parent provided, or made reasonable efforts to provide, the noncustodial parent with written notice of the revocation.

For tax years beginning after July 2, 2008 (the 2009 calendar year for most taxpayers), new rules apply to allow the custodial parent to revoke a release of claim to exemption that was previously released to the noncustodial parent on Form 8332, Release/Revocation of Release of Claim to Exemption for Child by Custodial Parent, or similar form. The revocation is effective no earlier than the tax year beginning in the calendar year following the calendar year in which the custodial parent provided, or made reasonable efforts to provide, the noncustodial parent with written notice of the revocation.

Economic Recovery Payment

Economic Recovery Payment

Making Work Pay

Making Work Pay

Making Work Pay TIP Nonresident aliens and taxpayers who can be claimed as dependents on someone else’s tax return are not eligible for the credit. Most Form W-2 wage earners have already benefited from the credit with a larger paycheck, as a result of the changes made to the federal income tax withholding tables in early 2009 (to implement the making work pay tax credit). The amount of the credit, however, must still be claimed on the taxpayer’s 2009 return (filed in 2010). Generally, Schedule M (Form 1040 A or 1040), Making Work Pay and Government Retiree Credits, is used to claim the credit.

Making Work Pay TIP Nonresident aliens and taxpayers who can be claimed as dependents on someone else’s tax return are not eligible for the credit. Most Form W-2 wage earners have already benefited from the credit with a larger paycheck, as a result of the changes made to the federal income tax withholding tables in early 2009 (to implement the making work pay tax credit). The amount of the credit, however, must still be claimed on the taxpayer’s 2009 return (filed in 2010). Generally, Schedule M (Form 1040 A or 1040), Making Work Pay and Government Retiree Credits, is used to claim the credit.

For homes purchased in 2009, taxpayers can qualify for a refundable credit of 10 percent of the purchase price up to $8, 000 ($4, 000 if Married Filing Separately). Generally, the credit for qualifying home purchases after December 31, 2008 and before December 1, 2009 do not have to be repaid, as long as the home remains the taxpayer's main home for 36 months after the purchase date. The amount of the credit begins to phase out for taxpayers whose modified AGI is more than $75, 000 ($150, 000 if Married Filing Jointly). For purposes of the credit, taxpayers are considered to be first-time homebuyers if they did not own any other main home during the threeyear period ending on the date of purchase.

For homes purchased in 2009, taxpayers can qualify for a refundable credit of 10 percent of the purchase price up to $8, 000 ($4, 000 if Married Filing Separately). Generally, the credit for qualifying home purchases after December 31, 2008 and before December 1, 2009 do not have to be repaid, as long as the home remains the taxpayer's main home for 36 months after the purchase date. The amount of the credit begins to phase out for taxpayers whose modified AGI is more than $75, 000 ($150, 000 if Married Filing Jointly). For purposes of the credit, taxpayers are considered to be first-time homebuyers if they did not own any other main home during the threeyear period ending on the date of purchase.

") Earned Income Credit (EIC)

Earned Income Credit (EIC)

") Earned Income Credit (EIC)

Earned Income Credit (EIC)

Investment Income

Investment Income

Advance EIC Payments

Advance EIC Payments