1f111cdd9ea21e8e75494807b4c82aa8.ppt

- Количество слайдов: 43

CHALLENGES & PLANS FOR DEMAND MANAGEMENT IN INDUSTIAL HUBS - A PRESENTATION BY HPSEB LTD. Venue: Baddi 2010 September 28,

CHALLENGES & PLANS FOR DEMAND MANAGEMENT IN INDUSTIAL HUBS - A PRESENTATION BY HPSEB LTD. Venue: Baddi 2010 September 28,

INDEX Ø Vision & Motto Ø HPSEB Ltd. – Responsibilities Ø HPSEB Ltd. – Existing Systems Ø Category Wise Consumption Ø Projected Demand Ø Future Plans & Turn Around Strategy Ø Availability of Adequate Power Ø Strengthening of EHV Systems in Industrial Hubs Ø Other Initiatives Ø Conclusions

INDEX Ø Vision & Motto Ø HPSEB Ltd. – Responsibilities Ø HPSEB Ltd. – Existing Systems Ø Category Wise Consumption Ø Projected Demand Ø Future Plans & Turn Around Strategy Ø Availability of Adequate Power Ø Strengthening of EHV Systems in Industrial Hubs Ø Other Initiatives Ø Conclusions

Vision & Motto ØTo be trusty and endearing public institution as an efficient provider of reliable and quality power at competitive rates on sustained basis (24 x 7, round the year) ØEnergizing and enhancing quality of lives and becoming a propeller for economic prosperity of State

Vision & Motto ØTo be trusty and endearing public institution as an efficient provider of reliable and quality power at competitive rates on sustained basis (24 x 7, round the year) ØEnergizing and enhancing quality of lives and becoming a propeller for economic prosperity of State

HPSEB LTD. - Responsibilities • In its reorganized form as a DISCOM (10. 6. 10) HPSEB Ltd. Has been entrusted mainly; • Distribution • Trading • O&M of existing Power House & Evacuation lines • Completion of Power Houses under construction & execution of projects so allocated by Go. HP.

HPSEB LTD. - Responsibilities • In its reorganized form as a DISCOM (10. 6. 10) HPSEB Ltd. Has been entrusted mainly; • Distribution • Trading • O&M of existing Power House & Evacuation lines • Completion of Power Houses under construction & execution of projects so allocated by Go. HP.

HPSEB LTD. – Existing Systems Installed capacity Villages Electrified Hamlets Electrified Consumer Connected Load EHV Sub Station Distribution Sub Station EHT Lines LT Lines Per Capita Consumption National Avg. = 467 MW = 17186 Nos. = 4623 Nos. = 19 Lakh = 4758101 k. W = 37 Nos. = 142 Nos. = 21302 Nos. = 2247 Ckt. Km = 28585 Ckt. Km = 53797 Ckt. Km = 937 KWh = 750 k. Wh

HPSEB LTD. – Existing Systems Installed capacity Villages Electrified Hamlets Electrified Consumer Connected Load EHV Sub Station Distribution Sub Station EHT Lines LT Lines Per Capita Consumption National Avg. = 467 MW = 17186 Nos. = 4623 Nos. = 19 Lakh = 4758101 k. W = 37 Nos. = 142 Nos. = 21302 Nos. = 2247 Ckt. Km = 28585 Ckt. Km = 53797 Ckt. Km = 937 KWh = 750 k. Wh

") Category wise Consumer (%)

Category wise Consumer (%)

") Category wise consumption (%)

Category wise consumption (%)

Peculiar Power Conditions in HP Ø Power in Himachal Pradesh is predominantly Hydro with the availability comprising of: ü Own Generation ( 100 % Hydro) – 467 MW ü Central Sector/bilateral shares (10 to 15% thermal) – total approx. 900 MW Ø This results in HPSEB being surplus in power during the summer months, and extreme deficits in winter months since ü Our own generation reduces almost to 15 - 25% due to lean water discharge ü Similar reduction happens with our Central Sector Shares from hydros in the region. ü There is an increase in demand due to the cold weather

Peculiar Power Conditions in HP Ø Power in Himachal Pradesh is predominantly Hydro with the availability comprising of: ü Own Generation ( 100 % Hydro) – 467 MW ü Central Sector/bilateral shares (10 to 15% thermal) – total approx. 900 MW Ø This results in HPSEB being surplus in power during the summer months, and extreme deficits in winter months since ü Our own generation reduces almost to 15 - 25% due to lean water discharge ü Similar reduction happens with our Central Sector Shares from hydros in the region. ü There is an increase in demand due to the cold weather

Monthly Demand (MU) 9") Our Annual Availability and Demand Pattern Monthly Availability (MU) Monthly Demand (MU) 9

Our Annual Availability and Demand Pattern Monthly Availability (MU) Monthly Demand (MU) 9

2009 -10 Winter Total There has been phenomenal growth") Demand Supply Scenario (in MU) 2009 -10 Winter Total There has been phenomenal growth in demand during last few years especially due to rapid industrialization resulting in reducing surpluses & increasing deficits. Description Summer Own Generation 1340. 08 396. 53 1736. 61 Baspa, IPPs Mini Micro including Patikari & Toss 1262. 96 291. 91 1554. 87 Central Sector with Unallocated Quota Bilateral Shares Total Availability Requirement within the State Surplus (+)/ Deficit (-) Additional Availability Unallocated Quota Go. HP Entitlements Forward Banking Contra Banking Purchase 1040. 55 440. 30 4083. 89 3951. 14 132. 75 1668. 55 626. 45 5586. 48 7042. 25 628. 00 186. 15 1502. 59 3091. 11 -1588. 52 320. 37 586. 06 365. 05 380. 04 Net Surplus (+)/ Deficit (-) 63. 00

Demand Supply Scenario (in MU) 2009 -10 Winter Total There has been phenomenal growth in demand during last few years especially due to rapid industrialization resulting in reducing surpluses & increasing deficits. Description Summer Own Generation 1340. 08 396. 53 1736. 61 Baspa, IPPs Mini Micro including Patikari & Toss 1262. 96 291. 91 1554. 87 Central Sector with Unallocated Quota Bilateral Shares Total Availability Requirement within the State Surplus (+)/ Deficit (-) Additional Availability Unallocated Quota Go. HP Entitlements Forward Banking Contra Banking Purchase 1040. 55 440. 30 4083. 89 3951. 14 132. 75 1668. 55 626. 45 5586. 48 7042. 25 628. 00 186. 15 1502. 59 3091. 11 -1588. 52 320. 37 586. 06 365. 05 380. 04 Net Surplus (+)/ Deficit (-) 63. 00

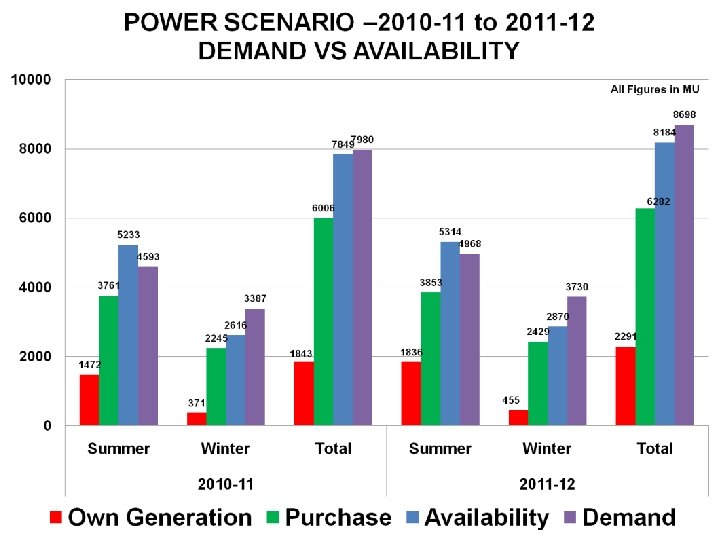

12660 11832 11500 MU 11058 10239 9481 9500 8698 7980 7500") Projected Demand (MU) 12660 11832 11500 MU 11058 10239 9481 9500 8698 7980 7500 2010 -11 2011 -12 2012 -13 Demand 2013 -14 2014 -15 2015 -16 2016 -17 11

Projected Demand (MU) 12660 11832 11500 MU 11058 10239 9481 9500 8698 7980 7500 2010 -11 2011 -12 2012 -13 Demand 2013 -14 2014 -15 2015 -16 2016 -17 11

Future Plans & Turn Around Strategy ü Adequate availability of cost effective power ü Strengthening of EHV, HV & LV Distribution System ü Reduction of T&D & AT&C Losses ü Reduction of Establishment Cost ü IT enabled environment for better human productivity and consumer services ü Accountability, Integrity & Transparency

Future Plans & Turn Around Strategy ü Adequate availability of cost effective power ü Strengthening of EHV, HV & LV Distribution System ü Reduction of T&D & AT&C Losses ü Reduction of Establishment Cost ü IT enabled environment for better human productivity and consumer services ü Accountability, Integrity & Transparency

AVAILABILITY OF ADEQUATE POWER – PROJECTIONS THEREOF

AVAILABILITY OF ADEQUATE POWER – PROJECTIONS THEREOF

Meeting the Growing Demand –Measures • Present Scenario: Ø Own Generation Ø Utilization of 100% Central Sector shares Ø Utilization of unallocated quota in Central Sector shares during winter months Ø Go. HP all entitlements in NJHPS & NHPC Projects during winter months Ø Purchase of power from existing SHPs Ø Power banking during monsoon for its return during winters Ø Availability of power through forward banking arrangements.

Meeting the Growing Demand –Measures • Present Scenario: Ø Own Generation Ø Utilization of 100% Central Sector shares Ø Utilization of unallocated quota in Central Sector shares during winter months Ø Go. HP all entitlements in NJHPS & NHPC Projects during winter months Ø Purchase of power from existing SHPs Ø Power banking during monsoon for its return during winters Ø Availability of power through forward banking arrangements.

Meeting the Growing Demand –Measures • Future Plans Ø Ø Ø Ø Ø Maximization of Own Generation Utilization of Go. HP entitlements in upcoming projects in the State when required Generation shares in HPPCL Projects against equity Purchase of power from up coming SHPs in the State Emphasis on enhanced unallocated quota in Central Sector generating stations. Emphasis on more quota in UMPPs. Power banking during monsoon for its return during winters Power purchase from IPPs for which Go. HP signed IAs Power purchase from open market/energy exchanges Endeavoring to ensure availability of 500 MW base power from Thermal/Gas stations during winter months. Ø Purchase of Power from open market

Meeting the Growing Demand –Measures • Future Plans Ø Ø Ø Ø Ø Maximization of Own Generation Utilization of Go. HP entitlements in upcoming projects in the State when required Generation shares in HPPCL Projects against equity Purchase of power from up coming SHPs in the State Emphasis on enhanced unallocated quota in Central Sector generating stations. Emphasis on more quota in UMPPs. Power banking during monsoon for its return during winters Power purchase from IPPs for which Go. HP signed IAs Power purchase from open market/energy exchanges Endeavoring to ensure availability of 500 MW base power from Thermal/Gas stations during winter months. Ø Purchase of Power from open market

Major projects under execution within the State Under HPSEBL: Sr. No. Project Installed Capacity (MW) Tentative Year of Commissioning HPSEBL’s Share %age MW 1 Bhabha Augmentation 4. 5 2010 -11 88 4 2 Ghanvi-II 10 2010 -11 88 9 3 Uhl-III 100 2011 -12 88 88 Total 101

Major projects under execution within the State Under HPSEBL: Sr. No. Project Installed Capacity (MW) Tentative Year of Commissioning HPSEBL’s Share %age MW 1 Bhabha Augmentation 4. 5 2010 -11 88 4 2 Ghanvi-II 10 2010 -11 88 9 3 Uhl-III 100 2011 -12 88 88 Total 101

Major projects under execution within the State Under Joint Venture/Central Sector: Sr. No. Project Installed Capacity (MW) Tentative Year of Commissioning HPSEBL’s Share %age MW 1 Chamera-III 231 2010 -11 17. 75 41 2 Koldam 800 2012 -13 17. 75 142 3 Parvati-III 520 2012 -13 17. 75 92 4 Parvati-II 800 2013 -14 17. 75 172 5 Rampur (HEP) 434 2014 -15 2. 47 11 6 Luhri (HEP) 775 2016 -17 2. 47 19 Total 477

Major projects under execution within the State Under Joint Venture/Central Sector: Sr. No. Project Installed Capacity (MW) Tentative Year of Commissioning HPSEBL’s Share %age MW 1 Chamera-III 231 2010 -11 17. 75 41 2 Koldam 800 2012 -13 17. 75 142 3 Parvati-III 520 2012 -13 17. 75 92 4 Parvati-II 800 2013 -14 17. 75 172 5 Rampur (HEP) 434 2014 -15 2. 47 11 6 Luhri (HEP) 775 2016 -17 2. 47 19 Total 477

Major projects under execution within the State Projects under HPPCL : Sr. Project No. Installed Tentative Year of HPSEBL’s Share Capacity (MW) Commissioning %age MW 1 Sawara Kudu 111 2012 -13 35. 2 39 2 Sainj 100 2015 -16 35. 2 35 3 Songtong Karchham 402 2015 -16 35. 2 142 4 Tidong 60 2013 -14 35. 2 21 5 Chirgoan Majgoan 42 2015 -16 35. 2 15 6 Kasang-I 65 2011 -12 35. 2 23 7 Kasang-II & III 130 2013 -14 35. 2 46 8 Kasang-IV 48 2014 -15 35. 2 17 9 Renuka Dam 40 2015 -16 35. 2 14 500 2014 -15 50 250 10 EMTA Power (Thermal) Total 602

Major projects under execution within the State Projects under HPPCL : Sr. Project No. Installed Tentative Year of HPSEBL’s Share Capacity (MW) Commissioning %age MW 1 Sawara Kudu 111 2012 -13 35. 2 39 2 Sainj 100 2015 -16 35. 2 35 3 Songtong Karchham 402 2015 -16 35. 2 142 4 Tidong 60 2013 -14 35. 2 21 5 Chirgoan Majgoan 42 2015 -16 35. 2 15 6 Kasang-I 65 2011 -12 35. 2 23 7 Kasang-II & III 130 2013 -14 35. 2 46 8 Kasang-IV 48 2014 -15 35. 2 17 9 Renuka Dam 40 2015 -16 35. 2 14 500 2014 -15 50 250 10 EMTA Power (Thermal) Total 602

Major Projects outside the State including UMPPs Sr. No. Project Installed Tentative Year of Capacity (MW) Commissioning HP’s Share 1 2 Barh-I (STPP) Barh-II (STPP( 1980 1320 2012 -13 %age 6. 58 1. 53 MW 130 20 3 North. Karanpura (STPP) 1980 2013 -14 1. 53 30 4 Rihand-III (STPP) 1000 2011 -12 3. 37 34 5 6 7 8 9 10 11 12 Meja (STPP) Lata Tapovan (HEP) Rupsiabagar (HEP) Kotibehl HEP (HEP) Vishnugarh (HEP) Koteshwar (HEP) Orissa-I (UMPP) Tamilnadu-II (UMPP) 1320 171 261 1045 444 4000 Total 2015 -16 2012 -13 2013 -14 2010 -11 2015 -16 2016 -17 3. 0 1. 53 2. 47 2. 01 fixed 40 3 4 26 8 8 100 45 448

Major Projects outside the State including UMPPs Sr. No. Project Installed Tentative Year of Capacity (MW) Commissioning HP’s Share 1 2 Barh-I (STPP) Barh-II (STPP( 1980 1320 2012 -13 %age 6. 58 1. 53 MW 130 20 3 North. Karanpura (STPP) 1980 2013 -14 1. 53 30 4 Rihand-III (STPP) 1000 2011 -12 3. 37 34 5 6 7 8 9 10 11 12 Meja (STPP) Lata Tapovan (HEP) Rupsiabagar (HEP) Kotibehl HEP (HEP) Vishnugarh (HEP) Koteshwar (HEP) Orissa-I (UMPP) Tamilnadu-II (UMPP) 1320 171 261 1045 444 4000 Total 2015 -16 2012 -13 2013 -14 2010 -11 2015 -16 2016 -17 3. 0 1. 53 2. 47 2. 01 fixed 40 3 4 26 8 8 100 45 448

Expected availabilities in next five years S. No Source 767 868 IPPs (PPAs with SHPs) 2. Expected MWs Own (Including Baspa) 1. Present MWs 140 500 -1000 Joint/Central Sector Shares Thermal, Gas & Others 750 1579 180 907 TOTAL 1837 MWs 3854 -4354 MWs Hydro

Expected availabilities in next five years S. No Source 767 868 IPPs (PPAs with SHPs) 2. Expected MWs Own (Including Baspa) 1. Present MWs 140 500 -1000 Joint/Central Sector Shares Thermal, Gas & Others 750 1579 180 907 TOTAL 1837 MWs 3854 -4354 MWs Hydro

14000 12000 POWER SCENARIO – 2012 -13 to 2013 -14 DEMAND VS AVAILABILITY 12323 10440 9950 9895 9666 10000 8374 8000 7522 6584 6456 5999 6000 5555 4666 4440 4111 4000 3949 3494 3311 2856 2373 2000 2373 1918 455 0 Summer Winter Own Generation 2012 -13 Total Purchase Summer Winter Total Availability Demand 2013 -14

14000 12000 POWER SCENARIO – 2012 -13 to 2013 -14 DEMAND VS AVAILABILITY 12323 10440 9950 9895 9666 10000 8374 8000 7522 6584 6456 5999 6000 5555 4666 4440 4111 4000 3949 3494 3311 2856 2373 2000 2373 1918 455 0 Summer Winter Own Generation 2012 -13 Total Purchase Summer Winter Total Availability Demand 2013 -14

18000 POWER SCENARIO – 2014 -15 to 2015 -16 DEMAND VS AVAILABILITY 16000 15570 14381 13884 14000 12998 11832 12000 11058 10778 9984 10000 9447 8822 8000 6758 6316 6000 5074 4792 4437 4742 4397 4177 4000 2373 1918 455 0 Summer Winter Own Generation 2014 -15 Total Purchase Summer Winter Total Availability Demand 2015 -16

18000 POWER SCENARIO – 2014 -15 to 2015 -16 DEMAND VS AVAILABILITY 16000 15570 14381 13884 14000 12998 11832 12000 11058 10778 9984 10000 9447 8822 8000 6758 6316 6000 5074 4792 4437 4742 4397 4177 4000 2373 1918 455 0 Summer Winter Own Generation 2014 -15 Total Purchase Summer Winter Total Availability Demand 2015 -16

STRENGTHENING OF EHV SYSTEMS IN INDUSTRIAL HUBS

STRENGTHENING OF EHV SYSTEMS IN INDUSTRIAL HUBS

Giri PSEB Jasoore Hamirpur Panchkula Bhakra Dehar Full Image

Giri PSEB Jasoore Hamirpur Panchkula Bhakra Dehar Full Image

Amb I & II (60 MW) Golthai/ Rakkar") Major Industrial Hubs Kandrori (16 MW) Amb I & II (60 MW) Golthai/ Rakkar (35 MW) Baddi-Barotiwala. Nalagarh area (290 MW) Paonta Sahib ( 40 MW) Kala –Amb (90 MW)

Major Industrial Hubs Kandrori (16 MW) Amb I & II (60 MW) Golthai/ Rakkar (35 MW) Baddi-Barotiwala. Nalagarh area (290 MW) Paonta Sahib ( 40 MW) Kala –Amb (90 MW)

re Pong-Jasoo 220 k. V Inter State Connection points Pan chk ula 220 Kunih ar k. V D eh 22 ar 0/ Ka 13 n 2 k go V o irpur Hoshiarpur-Ham 220 k. V ur irp am r-H ha k. V d an 220 Jal Kh od 22 ri-M 0 k ajr V i

re Pong-Jasoo 220 k. V Inter State Connection points Pan chk ula 220 Kunih ar k. V D eh 22 ar 0/ Ka 13 n 2 k go V o irpur Hoshiarpur-Ham 220 k. V ur irp am r-H ha k. V d an 220 Jal Kh od 22 ri-M 0 k ajr V i

Typical Summer Consumption Curve MW Peak Consumption > 900 MW Hours of the day

Typical Summer Consumption Curve MW Peak Consumption > 900 MW Hours of the day

Typical Winter Consumption Curve MW Peak Consumption > 1118 MW Hours of the day

Typical Winter Consumption Curve MW Peak Consumption > 1118 MW Hours of the day

1000 214 LUs 900 800") Load Curves for a Typical Day (14. 08. 10) 1000 214 LUs 900 800 MW 700 130 LUs 600 500 400 300 200 100 0 1 2 3 4 5 Total Demand 132/11 k. V Barotiwala-2 132 k. V GACL 6 7 8 Hour of the Day 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 220 k. V Baddi Uperla Nangal(Nalagarh) 132 k. V JP 132/66 k. V Barotiwala-1 132 k. V Kangoo (ACC) 132 k. V Paonta

Load Curves for a Typical Day (14. 08. 10) 1000 214 LUs 900 800 MW 700 130 LUs 600 500 400 300 200 100 0 1 2 3 4 5 Total Demand 132/11 k. V Barotiwala-2 132 k. V GACL 6 7 8 Hour of the Day 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 220 k. V Baddi Uperla Nangal(Nalagarh) 132 k. V JP 132/66 k. V Barotiwala-1 132 k. V Kangoo (ACC) 132 k. V Paonta

Strengthening of EHV Systems in Industrial Hubs Ø Infrastructure worth Rs. 1, 000 Crs has already been up to set state the in cater to the Industrial belts of the state Ø Another Rs. 900 Crs is being spent on augmenting/upgrading the infrastructure in the next two to three years…

Strengthening of EHV Systems in Industrial Hubs Ø Infrastructure worth Rs. 1, 000 Crs has already been up to set state the in cater to the Industrial belts of the state Ø Another Rs. 900 Crs is being spent on augmenting/upgrading the infrastructure in the next two to three years…

Strengthening of EHV Systems in Industrial Hubs Existing EHV Systems: Area Nalagarh Existing System Details 66/33 k. V 2 X 20 MVA, 66/11 k. V 2 X 20 MVA 80 Baddi 220/66 k. V 2 X 80/100 MVA 220/33 k. V 1 X 25/31. 5 MVA 231. 5 Barotiwala 132/66 k. V 3 X 31. 5 MVA 132/11 k. V 1 X 25/31. 5, 1 X 16 MVA, 1 X 16/20 MVA, 1 X 25/31. 5 MVA 173. 5 Paonta Sahib 132/33 k. V 1 X 25/31. 5 MVA, 1 X 16 MVA, 132/11 k. V 1 X 25/31. 5 99 Kala-Amb (i) 132/33 k. V 2 X 25/31. 5 MVA, (ii) 132/11 k. V 1 X 25/31. 5 MVA 94. 5

Strengthening of EHV Systems in Industrial Hubs Existing EHV Systems: Area Nalagarh Existing System Details 66/33 k. V 2 X 20 MVA, 66/11 k. V 2 X 20 MVA 80 Baddi 220/66 k. V 2 X 80/100 MVA 220/33 k. V 1 X 25/31. 5 MVA 231. 5 Barotiwala 132/66 k. V 3 X 31. 5 MVA 132/11 k. V 1 X 25/31. 5, 1 X 16 MVA, 1 X 16/20 MVA, 1 X 25/31. 5 MVA 173. 5 Paonta Sahib 132/33 k. V 1 X 25/31. 5 MVA, 1 X 16 MVA, 132/11 k. V 1 X 25/31. 5 99 Kala-Amb (i) 132/33 k. V 2 X 25/31. 5 MVA, (ii) 132/11 k. V 1 X 25/31. 5 MVA 94. 5

Strengthening of EHV Systems in Industrial Hubs Existing EHV Systems: Name Existing System Details Una (Amb I & II) 132/33 k. V 1 X 25/31. 5, 1 X 16 MVA 47. 5 Kandrori 132/33 k. V 2 X 16 MVA 32 Golthai & Rakkar 66/11 k. V 1 X 6. 3 MVA, 66 k. V feeder to Industry 6. 3 Pinjore Parwanoo Terrace 66/11 k. V 2 X 20 MVA 66/11 k. V 2 X 10 MVA TOTAL 40 20 824. 3

Strengthening of EHV Systems in Industrial Hubs Existing EHV Systems: Name Existing System Details Una (Amb I & II) 132/33 k. V 1 X 25/31. 5, 1 X 16 MVA 47. 5 Kandrori 132/33 k. V 2 X 16 MVA 32 Golthai & Rakkar 66/11 k. V 1 X 6. 3 MVA, 66 k. V feeder to Industry 6. 3 Pinjore Parwanoo Terrace 66/11 k. V 2 X 20 MVA 66/11 k. V 2 X 10 MVA TOTAL 40 20 824. 3

Strengthening of EHV Systems in Industrial Hubs Baddi-Barotiwala-Nalagarh Area Sr. No Name of Scheme 220/66 k. V, 2 x 100 MVA Substation at Uparala Nangal (Nalagarh) with 220 k. V line from PGCIL Nalagarh to Uparala Nangal (Nalagarh) 400/220 k. V 2 X 315 MVA Substation at Kunihar with 400 k. V line from Kunihar to 2 Nalagarh 220 k. V line from Uprala Nangal to Baddi with 220/66 k. V 1 x 100 MVA additional transformer at Baddi 66 k. V and 220 k. V line from Baddi to HIMUDA with 3 220/66 k. V 1 x 100 MVA Sub Station at Himuda with 4 transformer banks of 66/11 k. V 20 MVA each (To be further linked with Barotiwala and Parwano Sub Stations. 1 4 Addition of 220/33 k. V 1 x 25/31. 5 MVA Transformer at 220/66 k. V Sub. Station Baddi Addition of MVA 200 630 200 31. 5 5 66 k. V S/C line on D/C towers with Wold Conductor from 66 k. V Akkanwali Sub Station to Davni alongwith 33/11 k. V un-manned sub station at Davni near Nalagarh 6 Addition of 220/132 k. V, 1 x 100 MVA Transformer at Kunihar and 220 k. V line from Kunihar to Himuda 100 TOTAL 1161. 5

Strengthening of EHV Systems in Industrial Hubs Baddi-Barotiwala-Nalagarh Area Sr. No Name of Scheme 220/66 k. V, 2 x 100 MVA Substation at Uparala Nangal (Nalagarh) with 220 k. V line from PGCIL Nalagarh to Uparala Nangal (Nalagarh) 400/220 k. V 2 X 315 MVA Substation at Kunihar with 400 k. V line from Kunihar to 2 Nalagarh 220 k. V line from Uprala Nangal to Baddi with 220/66 k. V 1 x 100 MVA additional transformer at Baddi 66 k. V and 220 k. V line from Baddi to HIMUDA with 3 220/66 k. V 1 x 100 MVA Sub Station at Himuda with 4 transformer banks of 66/11 k. V 20 MVA each (To be further linked with Barotiwala and Parwano Sub Stations. 1 4 Addition of 220/33 k. V 1 x 25/31. 5 MVA Transformer at 220/66 k. V Sub. Station Baddi Addition of MVA 200 630 200 31. 5 5 66 k. V S/C line on D/C towers with Wold Conductor from 66 k. V Akkanwali Sub Station to Davni alongwith 33/11 k. V un-manned sub station at Davni near Nalagarh 6 Addition of 220/132 k. V, 1 x 100 MVA Transformer at Kunihar and 220 k. V line from Kunihar to Himuda 100 TOTAL 1161. 5

Strengthening of EHV Systems in Industrial Hubs Giri-Paonta-Kala Amb Area 1 220/132 k. V, 1 x 80/100 MVA Sub Station at Gondpur Aug. of 132/33 k. V transformers from 2 x 16 MVA to 2 x 25/31. 5 MVA and 2 replacement of 132/11 k. V, 16 MVA transformer bank with 1 x 25/31. 5 MVA at Paonta 3 Aug. of 132/33 k. V, 1 x 16/20 MVA transformer to 1 x 25/31. 5 MVA at 220 k. V Giri Sub Station 4 132 k. V, S/C line on D/C towers from Kala Amb to Moginand/Devani Providing 220 k. V D/C line from 220 k. V Giri nagar to Kunihar (Via Solan) with LILO at Jamta with 220 k. V D/C line from 220/132 k. V 100 MVA Sub 5 Station at Devni (For 220 k. V D/C line from Giri to Solan with conversion of 1 ckt of 132 k. V Giri Solan Kunihar Line) 100 46. 5 11. 5 100 6 132 k. V S/C line on D/C towers from Devni Sub Station to Kala Amb Aug. of 220/132 k. V, 2 x 63 MVA transformers to 2 x 80/100 MVA at Giri Sub Station at LILO of one Ckt of 220 k. V D/C Hatkoti-Moginand line at Giri Sub 7 Station TOTAL 258

Strengthening of EHV Systems in Industrial Hubs Giri-Paonta-Kala Amb Area 1 220/132 k. V, 1 x 80/100 MVA Sub Station at Gondpur Aug. of 132/33 k. V transformers from 2 x 16 MVA to 2 x 25/31. 5 MVA and 2 replacement of 132/11 k. V, 16 MVA transformer bank with 1 x 25/31. 5 MVA at Paonta 3 Aug. of 132/33 k. V, 1 x 16/20 MVA transformer to 1 x 25/31. 5 MVA at 220 k. V Giri Sub Station 4 132 k. V, S/C line on D/C towers from Kala Amb to Moginand/Devani Providing 220 k. V D/C line from 220 k. V Giri nagar to Kunihar (Via Solan) with LILO at Jamta with 220 k. V D/C line from 220/132 k. V 100 MVA Sub 5 Station at Devni (For 220 k. V D/C line from Giri to Solan with conversion of 1 ckt of 132 k. V Giri Solan Kunihar Line) 100 46. 5 11. 5 100 6 132 k. V S/C line on D/C towers from Devni Sub Station to Kala Amb Aug. of 220/132 k. V, 2 x 63 MVA transformers to 2 x 80/100 MVA at Giri Sub Station at LILO of one Ckt of 220 k. V D/C Hatkoti-Moginand line at Giri Sub 7 Station TOTAL 258

Strengthening of EHV Systems in Industrial Hubs Una-Rakkar-Tahliwala-Sansarpur Terrace Area 1 Aug. of 220/66 k. V 1 x 20 MVA Power Transformer to 40 MVA capacity in 220 k. V Switch Yard of Pong Dam HEP (BBMB) 20 2 Aug. of 132/33 k. V, 1 x 16 MVA transformer to 1 x 25/31. 5 MVA and 132/11 k. V, 1 x 16 MVA Trasnformer to 1 x 25/31. 5 MVA at Gagret Sub Station 31 3 Aug. of 132/33 k. V transformers at Una from 2 x 16 MVA to 2 x 25/31. 5 MVA 31 4 Replacement of one of 132/33 k. V, 16 MVA transformer with 1 x 25/31. 5 MVA at Amb. 15. 5 5 132 k. V, S/C line on D/C towers from Kandrori to Sansarpur Terrace alongwith 132/66 k. V, 31. 5 MVA Sub Station at Sansarpur Terrace 31. 5 6 132/33 k. V, 31. 5 MVA Sub Station at Tahliwala by providing 132 k. V S/C line on D/C tower from Una to Tahliwala. TOTAL 63 192

Strengthening of EHV Systems in Industrial Hubs Una-Rakkar-Tahliwala-Sansarpur Terrace Area 1 Aug. of 220/66 k. V 1 x 20 MVA Power Transformer to 40 MVA capacity in 220 k. V Switch Yard of Pong Dam HEP (BBMB) 20 2 Aug. of 132/33 k. V, 1 x 16 MVA transformer to 1 x 25/31. 5 MVA and 132/11 k. V, 1 x 16 MVA Trasnformer to 1 x 25/31. 5 MVA at Gagret Sub Station 31 3 Aug. of 132/33 k. V transformers at Una from 2 x 16 MVA to 2 x 25/31. 5 MVA 31 4 Replacement of one of 132/33 k. V, 16 MVA transformer with 1 x 25/31. 5 MVA at Amb. 15. 5 5 132 k. V, S/C line on D/C towers from Kandrori to Sansarpur Terrace alongwith 132/66 k. V, 31. 5 MVA Sub Station at Sansarpur Terrace 31. 5 6 132/33 k. V, 31. 5 MVA Sub Station at Tahliwala by providing 132 k. V S/C line on D/C tower from Una to Tahliwala. TOTAL 63 192

Strengthening of EHV Systems in Industrial Hubs Damtal-Kandrori Area 1 Addition of 132/33 k. V 1 x 16 MVA transformer at 132/33 k. V 2 x 16 MVA at Kandrori Sub Station. 16 Providing 220 k. V Ring Main System by constructing 220 k. V D/C Line Kangoo – 2 Mattansidh- Jassore with twin zebra conductor T 0 TAL 16

Strengthening of EHV Systems in Industrial Hubs Damtal-Kandrori Area 1 Addition of 132/33 k. V 1 x 16 MVA transformer at 132/33 k. V 2 x 16 MVA at Kandrori Sub Station. 16 Providing 220 k. V Ring Main System by constructing 220 k. V D/C Line Kangoo – 2 Mattansidh- Jassore with twin zebra conductor T 0 TAL 16

Expected Existing S. No Name of") Expected Transformation Capacities (in Next 2 -3 years) Expected Existing S. No Name of the Area Transformation Capacities (MVA) 1. Parwanoo-Baddi. Barotiwala-Nalagarh 525 1646. 5 2. Giri-Paonta-Kala-Amb 193. 5 451. 5 3. Una-Rakkar-Tahliwala -Sansarpur Terrace 73. 8 265. 8 4. Damtal-Kandrori 32 48 821. 3 2411. 8 TOTAL

Expected Transformation Capacities (in Next 2 -3 years) Expected Existing S. No Name of the Area Transformation Capacities (MVA) 1. Parwanoo-Baddi. Barotiwala-Nalagarh 525 1646. 5 2. Giri-Paonta-Kala-Amb 193. 5 451. 5 3. Una-Rakkar-Tahliwala -Sansarpur Terrace 73. 8 265. 8 4. Damtal-Kandrori 32 48 821. 3 2411. 8 TOTAL

220/132 k. V=2 x 80/100 MVA 132/33 k. V = 1 x 8 MVA 100 MVA 400 k. V Kuniha r 132/66/11 k. V Baroti -wala 220/132/ 33 k. V Kunihar 132/66 k. V=3 x 31. 5 MVA 132/11 k. V =31. 5*2+16*1+20*1 Capacity = 193. 5 220/132/66/3 3 k. V Baddi 132/6 6/33 k. V Solan 220/66 k. V Uparla Nangal (2 x 80/100) MVA 100 MVA 220 k. V Panchku la -Baddi Line Panchkula 220/132 k. V = 2 x 80/100 MVA 220/33 k. V = 1 x 25/31. 5 MVA 66/33 k. V= 1 x 20 MVA 66/11 k. V = 4 x 20 KVA 132/66 k. V=1 x 31. 5 MVA 132/33 k. V=1 x 50 MVA 132/33 /11 KV Poanta Sahib From Khodri (Uttaranchal) Giri 220/ 132 k. V Devani 132/33 k. V = 2 x 25/31. 5 MVA 132/11 k. V = 2 x 25/31. 5 MVA 132/33 /11 k. V Kala Amb 400/220 k. V Nalagarh (Powergrid) 2 x 315 MVA GIRI HEP ~ Total capacity available Baddi/Barotiwala) 493 Total capacity available (Giri/KAmb/Paonta) 215 Addl capacity proposed in Baddi/Barotiwala 270 Addl capacity proposed in Giri/K- 215. 5

220/132 k. V=2 x 80/100 MVA 132/33 k. V = 1 x 8 MVA 100 MVA 400 k. V Kuniha r 132/66/11 k. V Baroti -wala 220/132/ 33 k. V Kunihar 132/66 k. V=3 x 31. 5 MVA 132/11 k. V =31. 5*2+16*1+20*1 Capacity = 193. 5 220/132/66/3 3 k. V Baddi 132/6 6/33 k. V Solan 220/66 k. V Uparla Nangal (2 x 80/100) MVA 100 MVA 220 k. V Panchku la -Baddi Line Panchkula 220/132 k. V = 2 x 80/100 MVA 220/33 k. V = 1 x 25/31. 5 MVA 66/33 k. V= 1 x 20 MVA 66/11 k. V = 4 x 20 KVA 132/66 k. V=1 x 31. 5 MVA 132/33 k. V=1 x 50 MVA 132/33 /11 KV Poanta Sahib From Khodri (Uttaranchal) Giri 220/ 132 k. V Devani 132/33 k. V = 2 x 25/31. 5 MVA 132/11 k. V = 2 x 25/31. 5 MVA 132/33 /11 k. V Kala Amb 400/220 k. V Nalagarh (Powergrid) 2 x 315 MVA GIRI HEP ~ Total capacity available Baddi/Barotiwala) 493 Total capacity available (Giri/KAmb/Paonta) 215 Addl capacity proposed in Baddi/Barotiwala 270 Addl capacity proposed in Giri/K- 215. 5

Other Initiatives • Under R-APDRP Programme of Govt. of India, 14 Nos. Towns of Himachal Pradesh have been identified. – Under Part-A the IT enabled environment is being created in these town which will set the base line data right for demonstrable improvement and increase the human productivity & enhanced consumer satisfaction. – Under Part-B renovation modernization and strengthening of electrical systems, feeder segregation etc. is being undertaken, which shall result in; • • • Reduction of T&D Losses Bring Commercial Viability Reduction of outages and interruption Increase consumer satisfaction Increased availability

Other Initiatives • Under R-APDRP Programme of Govt. of India, 14 Nos. Towns of Himachal Pradesh have been identified. – Under Part-A the IT enabled environment is being created in these town which will set the base line data right for demonstrable improvement and increase the human productivity & enhanced consumer satisfaction. – Under Part-B renovation modernization and strengthening of electrical systems, feeder segregation etc. is being undertaken, which shall result in; • • • Reduction of T&D Losses Bring Commercial Viability Reduction of outages and interruption Increase consumer satisfaction Increased availability

scheme worth Rs. 87. 65 Cr. Has been") Other Initiatives • Under R-APDRP (Part-B) scheme worth Rs. 87. 65 Cr. Has been submitted to Govt. of India for appraisal and approval, which comprises of following main activities: – Addition of 2 Nos. 66/11 k. V, 2 x 20 Mv. A Sub Station at Baddi and Manpura and 3 No. additional transformers of capacity 20 MVA each at 66/33/11 k. V Akanwali, Davni & Himuda – HVDS comprising of 75 Nos. DTRs alongwith LT lines – Augmentation/Re-conductoring HT & LT System and addition of new DTRs – Installation of Capacitor Banks etc.

Other Initiatives • Under R-APDRP (Part-B) scheme worth Rs. 87. 65 Cr. Has been submitted to Govt. of India for appraisal and approval, which comprises of following main activities: – Addition of 2 Nos. 66/11 k. V, 2 x 20 Mv. A Sub Station at Baddi and Manpura and 3 No. additional transformers of capacity 20 MVA each at 66/33/11 k. V Akanwali, Davni & Himuda – HVDS comprising of 75 Nos. DTRs alongwith LT lines – Augmentation/Re-conductoring HT & LT System and addition of new DTRs – Installation of Capacitor Banks etc.

Conclusions q HPSEBL is committed to provide adequate, reliable power to all its consumers and in this direction all out efforts are afoot. q HPSEBL is also committed to ensure Grid discipline & operate with in a frequency band of 49. 5 Hz to 50. 2 Hz. To achieve the above aims we seek the support & cooperation of our Industrial brethren.

Conclusions q HPSEBL is committed to provide adequate, reliable power to all its consumers and in this direction all out efforts are afoot. q HPSEBL is also committed to ensure Grid discipline & operate with in a frequency band of 49. 5 Hz to 50. 2 Hz. To achieve the above aims we seek the support & cooperation of our Industrial brethren.

THANK YOU

THANK YOU