275eb2668c6cca8fbee9118261c9a5e9.ppt

- Количество слайдов: 42

CEO Series Marine Insurance Essentials by Professor Alkis John Corres

Ships and cargoes have been insured for centuries against marine perils. • This presentation intends to present the salient features of marine insurance with particular reference to cargo carrying vessels. • The two principal types of insurance provided for merchant ships are Hull & Machinery (H&M) and Protection and Indemnity (P+I). • H&M insurance will provide compensation to ship owners in case of ship damage or loss. • P+I cover will protect and indemnify owners against claims from third parties. • The two together form a powerful system of insurance that no ship owner under any circumstances should be without for any length of time.

PART ONE Hull & Machinery Insurance

Marine Insurance provides cover in case of loss or damage. The classic distinction is between ship and cargo insurance, however marine insurance covers a wider area. • This area includes also terminals, storage depots and other means of transport between loading and final destination of the cargo. • The part that concerns us at this time is primarily ship insurance and secondarily cargo insurance. • Marine insurance is a very old type of insurance dating back to ancient Greek and Roman times. In its contemporary form it has been closely associated with the advent of a specialist insurance market in London and the final form of the Marine Insurance Act (1906). • Marine insurance has benefitted from the use of standard clauses developed by the Institute of London Underwriters.

Marine insurance is arranged through brokers who work on a commission basis between the contracting parties who are the owners of the vessel on one hand, and the underwriters on the other. The role of the insurance broker is pivotal in marine insurance being the interface between two different areas of economic activity and it has played an important part in the development of the City of London as an international insurance hub. Vessel Owners (Insured) Insurance Broker Underwriters

Hull & Machinery cover provides insurance protection for the vessel and traditionally it has been offered by ‘’Underwriters” each one of who insure only a small portion of the risk and together cover 100% of the ship’s contract. • Hull & Machinery policies can be provided for a specific voyage, or – much more often - for an agreed time period, usually one year. A yearly renegotiation allows, among other reasons, for changes in terms and in the market value of the vessel. • The legal basis for these is the Marine Insurance Act (1906) and its standard form (the SG form) as it has been reworked in 1991 by the London Market to include the Institute Clauses (MAR 91). • The losses covered include Total Loss and Partial Loss unless otherwise agreed ( typically TLO contracts where partial losses are not covered). • Historically, underwriters have been individuals (referred to as Names) but corporate underwriting has been on the increase. • The liability of underwriters towards the owners is joint, but not several.

The distinction between the various types of loss can be summarized diagrammatically as follows: Actual Total Loss Constructive Total Loss Marine Insurance (H&M) Particular Average Partial Loss General Average

The successful conclusion of negotiations through the insurance broker leads to the issuance of a Cover Note. • The cover note is a temporary document. Insurance companies issue a cover note in order to provide owners with proof of insurance before all the insurance paperwork has been finalized. • Upon conclusion of the paperwork the insurer issues the policy document and the certificate of insurance. • In general, the cover note provides the same level of coverage as the full insurance policy (although insurers may make minor changes while they make the final determinations on the risks associated with the insurance policy). • The presentation of a cover note to an interested party e. g. a lending bank, is sufficient proof that the vessel is covered by insurance until the full text policy document and the certificate of insurance become available.

Marine Insurance has been designed to provide cover for marine perils. Marine perils are perils consequent on, or incidental to the navigation of the sea. Perils of the Sea make reference to all risks particular to the sea. Marine Perils of the Sea Losses emanating from the Perils of the Sea cannot generally be foreseen or be prevented by competence or by exercise of reasonable care by the seaborne staff.

Marine Perils – other than the perils of the sea – are shown below and have a wider scope providing cover for the following. Jettison (dumping) of the cargo. It has to be intentional. Detention of vessel and cargo in port due to blockage or quarantine, (not Port State Control). Damage by fire, explosion, combustio n etc excluding willful misconduct. Barratry: Willfully conducted act by an officer or crew against ship or cargo. Men-of-War covers losses incurred by collision with a vessel employed by a state for defense or attack. Acts of Pirates, rovers, thieves (less frequent in modern times). Taking at sea covers losses incurred by stopping a vessel and taking it into port for investigation suspecting illegal acts. Enemies cover against hostile acts performed by an enemy. Restraints are preventions to free use of a port causing delays and other losses. Letter of Mart/ Counter Mart refers to powers vested on an individual by a government to attack merchant vessels. Arrest makes reference to taking away the vessel by force, not a judicial arrest. Other perils i. e. perils of a similar nature, or consequent to any of the above.

Marine insurance contracts typically include an amount of money called ‘’deductible’’, also known as ‘’excess’’, which the insured will be asked to pay first in case of a loss. Payment by the underwriters will follow, or same will be reduced by that amount if unpaid by owners. • It follows that the higher the amount of the deductible, the cheaper the cost of the insurance policy as owners accept to self insure for the initial part of the loss. • Another point that needs to be understood is that in cases of: Ø Collision with another vessel (Running Down Clause), and Ø Wreck removal, the underwriters will cover 3/4 ths of the loss, the remaining part to be covered by the P+I of the vessel, (unless the policy is amended to 4/4 ths). For example: In case of a collision with another ship resulting to losses of say $ 1 million for the insured vessel, the underwriters will be under obligation to pay $750, 000 minus the deductible (say, $ 50, 000) i. e. $700, 000, and the P+I will pick up the bill for the outstanding $ 300, 000.

Unless the policy otherwise provides, the insurer is liable for losses proximately caused by a peril insured against. • On the contrary, the insurer is not liable : Ø If the loss is caused by a peril not insured against. Ø In case of a breach of an – express or implied – warranty by the insured e. g. seaworthiness, Ø If the loss is caused by delay, which is caused by a peril insured against. Ø If the loss is caused by ordinary wear & tear, ordinary leakage or breakage, Ø If the insured voyage is illegal.

A loss may be either total or partial. Unless otherwise agreed vessels covered for Total Loss are also covered for Partial Loss. Any loss other than Total is Partial loss. There is no third option. A Total Loss can be either: Actual total loss, or Constructive total loss.

the vessel is actually")

ACTUAL TOTAL LOSS An actual total loss occurs when: (a) the vessel is actually destroyed or irreparably damaged, and, (b) the vessel ceases to be a thing of the kind insured, and, (c) the assured is irretrievably deprived of the vessel.

CONSTRUCTIVE TOTAL LOSS A constructive total loss occurs when the ship insured: q is reasonably abandoned because its actual total loss appears to be unavoidable, or (more frequently), q in case the cost of repairs plus the cost of salvage will exceed its insured value. In CTL there is remaining property, unlike in cases where the ship is lost at sea, or it has been subject to theft.

PARTIAL LOSS CAN BE EITHER a Particular Average, or a General Average. There can be no third option. • Particular Average is a partial loss to the vessel, caused by a peril insured against, which is not a General Average loss. • In Particular Average there can be no contribution to the loss from the cargo side as in the case of General Average. • Examples of particular average are grounding damage, main engine damage during voyage, heavy weather damage, fire onboard etc. • Particular Average has a accidental nature and not the intentional character necessary to qualify as a General Average claim.

PARTIAL LOSS CONTINUED… • General Average exists when extraordinary sacrifices are made at the time of peril to save the common adventure. It calls for: o Voluntary sacrifice. o Serious and imminent danger. o The adventure must actually be imperiled, (sacrifice in anticipation is not recognized as GA), and the o Objective of the sacrifice must be the preservation of adventure. o ----------------------o Sometimes the dividing line between Particular Average and General Average in a single incident needs to be carefully assessed. For example, while the grounding of a vessel is clearly a PA claim, the compensation of salvors to refloat it is a GA claim due to its voluntary nature and the cargo side will have to contribute to it.

PARTIAL LOSS CONTINUED…EXAMPLES OF GA • • General Average is adjusted according to the York – Antwerp Rules by average adjusters who are specialized professionals acting as individuals or as part of a corporate structure. The appointment of an Average Adjuster is made by the owners of the vessel and the cost of his services is covered by the underwriters. The first object of work of an average adjuster will be the calculation of the Value at Risk, to be followed by the apportionment of the GA among the parties participating in the marine adventure i. e Hull, Cargo, Freight and Bunkers.

There are other specialist insurance policies available on request catering for different requirements. • • Increased Value (otherwise known as Hull Interest/Disbursements/Freight Interest) insurance provides cover to the owners in case of a claim when there is a difference between the insured value and the market value of the ship (usually within a margin of 20%). It kicks in following a declaration of a total loss and it can also include GA, Sue and Labour expenses and Excess Collision liability. A Freight Interest policy insures against the loss of anticipated future earnings of the vessel following total loss, going beyond the scope of a classic Loss of Hire policy. I. V. is popular with bareboat charterers, professional ship management companies and ship owners.

Specialist insurance policies…continued • A Loss of Hire policy is interesting to owners, lenders, time charterers and bareboat charterers as it covers losses incidental to partial loss (rather than total loss covered by H&M) usually for a time period from 3 -6 months after the incident. • The losses covered include daily running costs following an incident and loss of earnings. Charterers can also insure themselves against increased cost of charter following an incident which temporarily impairs the operational ability of a vessel. • Loss of hire policies do not start immediately after the incident, they usually start two to four weeks after the incident and tend to be rather pricey.

Specialist insurance policies…continued • Mortgagee Interest & Additional Perils. This specialist policy is designed to protect the interests of lenders, banks and other financial institutions in case of refusal to pay on the part of underwriters, usually following a breach of warranty by the insured. • The Additional Perils part pertains to pollution liability claims and expenses which exceed the P+I limits (which nevertheless are quite high and difficult to exceed). • Banks insist this policy is bought and paid in every financing deal they do by the borrowers alongside the classic H&M and P+I policies they require to see concluded. • The owners of vessels given out to bareboat charters may also require from the bareboat charterers to take out this policy.

Specialist insurance policies…continued • • War Risks cover is applicable in cases when a ship enters into a war zone where common insurance policies cease to apply. Underwriters need to be advised strictly 48 hours before the ship enters in such areas and not earlier. Upon receipt of such advice they will be advising the insured about the list of exclusions applicable and the additional premium. These policies offer protection to owners against war-related perils and terrorism and typically have no deductible. The risks they protect against are generally not covered by H&M insurance therefore War Risk cover is bought separately. (Some of these perils are restraint, capture, confiscation, arrest, detainment etc). Marine War policies will terminate in case of war between major powers. War zones are declared by the Joint War Committee and may additionally include piracy problem areas. On the cargo side there is a vast variety of policies which are underwritten on basis of the Institute Cargo Clauses at three levels of coverage. This part of marine insurance is outside the scope of this presentation.

END OF PART ONE

PART TWO P+I Insurance

P+I insurance has a mutual character and there are no underwriters as in H&M. P+I clubs are associations and instead of shareholders, they have members who pay calls and receive cover. It follows that P+I clubs cannot pay dividend any surplus of income over expenses remains in the club. When one offers a service for reward or third parties use his facilities, there is always an exposure to claims should something go wrong. The same liability regime applies to carriers, shipowners or operators. The main areas of risk covered by a P+I club are: Ø Crew claims: (injury/illness/death/repatriation/substitution cost/deviation) Ø Collision & Wreck removal (25% thereof) Ø Damage to fixed and floating objects/docks/coral reefs Ø Marine Pollution/cleanup/damages Ø Cargo damage/shortage Ø Fines Ø Stowaways Ø Other

P+I mutual insurance associations date back to the middle of the 19 th century. The P+I concept is quite straightforward, members regularly pay to the club money (Advance Call) and out of the accumulated funds the club covers the liability of its members towards third parties against a plethora of risks. In case a member wishes to leave his P+I club he will be requested to pay before leaving a sum (Release Call). ‘’The intent of release calls is to remove any potential future liability for further calls to the club following termination of membership in the particular club. By paying the release call, the member is ‘released’ from their obligation to pay future supplementary calls to the club. Thus the release call is intended to represent the member’s proportion of the club’s incurred but not reported (IBNR) claims for the open years outstanding. ’’ (Willis).

The International Group of P+I Clubs. • • ‘’The history behind the IGA is also the history of the Pooling Agreement which has its origins back in 1899. Then, the so-called London Group of P&I Clubs, which at that time consisted of six Clubs, entered into the first claims sharing agreement. The principal purpose of the Pooling Agreement was the same then as it is today. It constituted the legal framework for claims sharing among the Group Clubs. Only later, in 1951, did it become also the vehicle for the collective purchase of market reinsurance cover. ’’ (GARD, The International Group Agreement). Today, the reinsurance contract of the International Group is the biggest reinsurance contract in the world and it offers the necessary confidence to everyone involved directly, or otherwise, in international seaborne trade.

Club business is separated in policy years within which club income should cover all the liabilities of the club’s members. • In cases where club’s income falls short of obligations within a policy year – something that becomes known two to three years later when claims settlement is completed – members are asked to pay a supplementary call, or ’’back call’’ i. e. an additional amount to balance the club’s books for that policy year. • In the opposite case, the surplus can be saved to address future claims, or to balance deficits in previous policy years • Clubs are managed by professional managers overseen by a board of directors chosen usually from their members. Managers deal with almost everything as long as it falls within the Club Rules. • Matters falling outside the club rules and other high financial impact issues end up in the agenda of the club’s board. • Changes in a club’s rules are voted on by all its members in general assemblies.

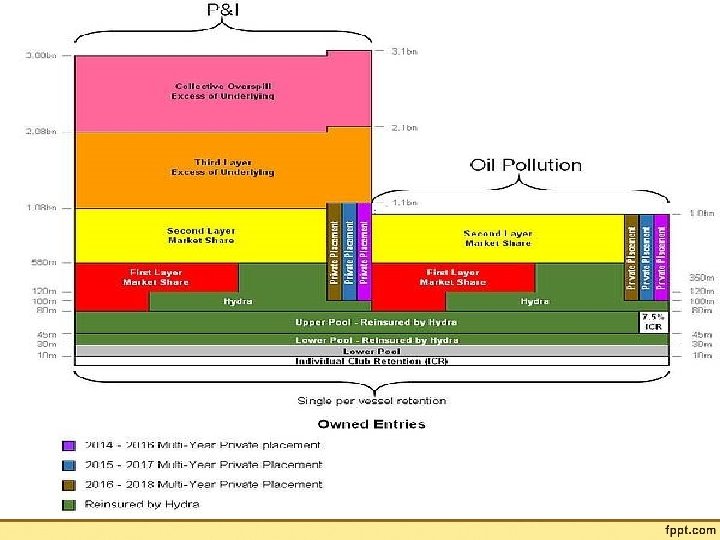

Claims’ sharing lies at the heart of the P+I system. Claims are dealt with in three tranches. • • • The first tranche – as of 2016 policy year - is retained by the club to which the claiming vessel is a member for claims up to $ 10 million including a reinsurance premium (abatement) to cover claims between $ 3 – 10 million. Claims which exceed the above limit fall in the second tranche and are dealt with by all the International Group clubs together up to a limit of $ 80 million. The second tranche is divided in two Pools, Lower Pool $ 10 -45 million, and Upper Pool $ 45 -80 million (the claiming club retaining 7. 5% of the claim across the two pools). Finally, very big claims exceeding the second tranche’s Upper Pool limit ($80 million), are covered by the third tranche (reinsurance) under the Excess of Loss Programme and a subsidiary reinsurance facility under the name Hydra.

Individual member’s premium calculation and reinsurance cost. • The money paid by an individual company to a club (premium) is calculated: Ø a. on basis of the club’s overall exposure to the fleet (age/type/GT/trade) and Ø b. on the individual member’s claims record (below $ 3 million). Reinsurance cost 2016/17 rates summary 2016 rate per GT% change from 2015 • DIRTY TANKERS $ 0. 6567% - 10. 25 • CLEAN TANKERS $ 0. 2816% - 10. 26 • DRY CARGO VESSELS $ 0. 4537% - 7. 18 • PASSENGER VESSELS $ 3. 5073%* -7. 19 • CHART TANKERS $ 0. 2380% -5. 63 • CHART DRIES $ 0. 1163% -5. 29 Source: International Group Reinsurance Update January 2016 * The passenger ships’ rate reflects the claims from the Costa Concordia accident.

The P+I number of claims has been showing a steady decline between 2006 and 2015. • This evidences the long term benefits of IMO initiatives in all fronts (ISM Code, STCW, etc) as well as the overall quality increase in the services rendered by the world fleet. • Individual club retention has steadily risen over that period to USD 10 million from about 6 million in 2006. • The reduced number of claims has also had a positive impact on reinsurance and it has allowed for favourable renewal terms plus an extension of cover as of 20 th February 2016 to include nuclear risk liabilities arising out of approved certificates, guarantees, or undertakings up to a limit of US $ 1 billion. Such liabilities were not covered previously.

Typical factors considered by clubs for assessing a member’s risk. A. SHIP Type of vessel Types of operations Reefer/Drilling/Towage Age of Vessel Machinery employed Class Flag National or Flag of Convenience Trading Crew (Nationality/Qualifications)

Factors considered…continued. B. OPERATOR Experience in trade operations Nationality of the assured Owners/Managers/Charterers Loss Record – Adverse claims record Previous Insurers (P+I Club) Size of fleet Extent of cover required.

In a nutshell, a P+I club does many things to make the life of owners, managers and crews safer and easier. The club manages claims v It acts as central point of contact and it appoints experts, lawyers and correspondents through its worldwide network v It provides 24 hour emergency response v It pays claims and fees incurred v It advises on safety and loss prevention i. e. it issues circulars to members, aimed at reducing incidents that may result in a claim. It also provides operational security Ø Deals with arrest or threat of arrest of an entered ship Ø Issues club letters of undertaking and pollution cover cards Ø Arranges for bank guarantees Ø It is useful in a million ways to the assured.

Time frame of a P+I claim. It involves in principle in four stages. Phase 1: Notification about the incident / initial handling (five hours). Parties to be notified include: § Authorities, § agents, § insurers (P&I - H&M - loss of hire), § charterers, cargo interests. The aim is to direct and co-ordinate initial response including the handling of media (critical in passenger ship accidents and marine pollution incidents).

Time frame of a P+I claim in four stages… Phase 2: Management of the incident (about one week), Dealing with the on-going crisis, assistance to master / crew, local office, local authorities, pollution. Response co-ordination with port authorities, government organizations, central point of contact, arrange mobilization of resources, teamwork, claimants/security, media/press handling. Minimization of risk. Gathering and preserving evidence, investigating source and cause of incident, recording time sequence of events, taking crew statements, ship’s logs, obtaining documents, video of incident / photographs of accident site, retaining any relevant equipment or evidence, monitoring surveyors from third parties and restricting access where necessary.

Time frame of a P+I claim in four stages… Phase 3: Legal and technical assessments (about three months), i. e. v liability analysis, v jurisdiction, applicable law, v estimation of the extent of damage, v joint strategy together with the member.

Time frame of a P+I claim in four stages… Phase 4: Final settlement(about three years), including but not limited to: legal proceedings, settlement negotiations and final resolution of all outstanding claims.

End of the presentation and thank you for your attention. Any questions?

275eb2668c6cca8fbee9118261c9a5e9.ppt