9d65f2301785216d2214711e691abbb3.ppt

- Количество слайдов: 17

Capitalization of R&D in the national accounts of Israel

Capitalization of R&D in the national accounts of Israel

The exercise performed to test: • Feasibility of using existing R&D statistics as a basis for estimates of R&D assets in national accounts. • Implementation of recommendations developed in the framework of the Canberra II group during the last 4 years. • Examination of the impact of R&D capitalization on the main national accounts aggregates.

The exercise performed to test: • Feasibility of using existing R&D statistics as a basis for estimates of R&D assets in national accounts. • Implementation of recommendations developed in the framework of the Canberra II group during the last 4 years. • Examination of the impact of R&D capitalization on the main national accounts aggregates.

Bridge tables between R&D statistics and national accounts Bridging values needed: • Acquisition of “extramural” R&D to be used as input in R&D production • Consumption of fixed capital owned by R&D producers and used in R&D production • Net operating surplus • Other taxes on production less other subsidies on production

Bridge tables between R&D statistics and national accounts Bridging values needed: • Acquisition of “extramural” R&D to be used as input in R&D production • Consumption of fixed capital owned by R&D producers and used in R&D production • Net operating surplus • Other taxes on production less other subsidies on production

Table 1. Summary of simplified bridge table results for Israel

Table 1. Summary of simplified bridge table results for Israel

Estimates of R&D capital formation • Supply and use of R&D output using the data from bridge tables. • Distinction between market and nonmarket R&D. • Separation of exports and imports of R&D proved to be important. • Constant price estimates prepared in satellite accounts since 1989.

Estimates of R&D capital formation • Supply and use of R&D output using the data from bridge tables. • Distinction between market and nonmarket R&D. • Separation of exports and imports of R&D proved to be important. • Constant price estimates prepared in satellite accounts since 1989.

• Time lag between the start of") Estimates of R&D capital formation (contd. ) • Time lag between the start of R&D projects and the use of the finalized R&D - gestation lag and application lag – assumed to be 2 years, basing on venture capital funds sources. • Unfinished R&D defined as stocks of work in progress, considering the high share of R&D exports in Israel.

Estimates of R&D capital formation (contd. ) • Time lag between the start of R&D projects and the use of the finalized R&D - gestation lag and application lag – assumed to be 2 years, basing on venture capital funds sources. • Unfinished R&D defined as stocks of work in progress, considering the high share of R&D exports in Israel.

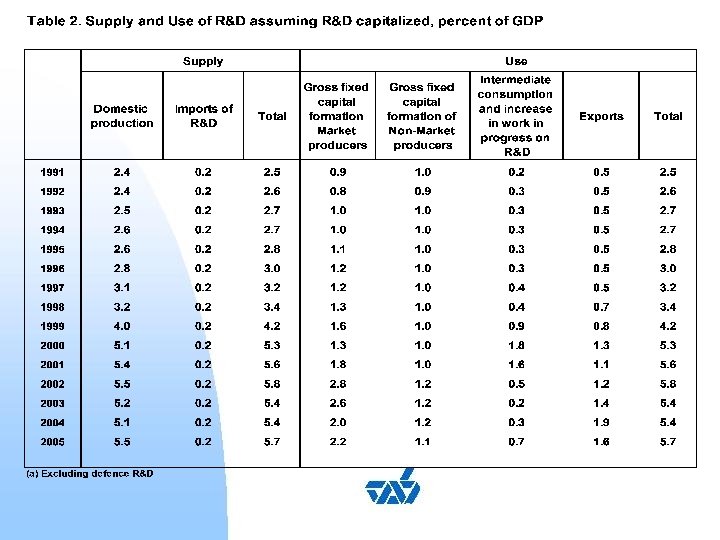

Uses of R&D at 2000 prices

Uses of R&D at 2000 prices

Estimates of service lives of R&D • Original intention to estimate service lives of R&D in Israel using existing panel data was abandoned due to lack of some important variables. • Instead, an average depreciation rate of 0. 15, derived from the paper by Ballester, Garcia-Ayuso, Livnat (2000). • In future work it will be necessary to improve the service life estimates, i. a. , by performing industry depreciation rates.

Estimates of service lives of R&D • Original intention to estimate service lives of R&D in Israel using existing panel data was abandoned due to lack of some important variables. • Instead, an average depreciation rate of 0. 15, derived from the paper by Ballester, Garcia-Ayuso, Livnat (2000). • In future work it will be necessary to improve the service life estimates, i. a. , by performing industry depreciation rates.

Estimates of R&D capital stocks

Estimates of R&D capital stocks

Net impact of capitalization of market R&D on GDP

Net impact of capitalization of market R&D on GDP

Net impact of capitalization of market and non-market R&D on GDP

Net impact of capitalization of market and non-market R&D on GDP

Capital formation compared to depreciation • Net GFCF obtained is continuously positive, since the depreciation is lower than the fixed capital formation in most years, due to relatively fast growth of the GFCF over the years. • However, the actual impact of R&D capitalization on NDP and NNI is different, since other changes to registration of output for final use have also been made.

Capital formation compared to depreciation • Net GFCF obtained is continuously positive, since the depreciation is lower than the fixed capital formation in most years, due to relatively fast growth of the GFCF over the years. • However, the actual impact of R&D capitalization on NDP and NNI is different, since other changes to registration of output for final use have also been made.

Net fixed capital formation in R&D compared to NNI at market prices

Net fixed capital formation in R&D compared to NNI at market prices

Conclusions from the exercise • Feasible to integrate R&D statistics in national accounts, and obtain R&D capital formation and stocks. • The impact of capitalizing market R&D amounts to about 1. 5% of GDP • The impact of non-market R&D is also significant - about 1. 0% of GDP.

Conclusions from the exercise • Feasible to integrate R&D statistics in national accounts, and obtain R&D capital formation and stocks. • The impact of capitalizing market R&D amounts to about 1. 5% of GDP • The impact of non-market R&D is also significant - about 1. 0% of GDP.

• The treatment of non-market R&D in this") Conclusions from the exercise (contd. ) • The treatment of non-market R&D in this way is consistent with the treatment of roads and other infrastructure in the current SNA. • However, it is important to show such R&D separately, since it is used by other sectors. • Although the individual use mostly can not be identified, the scope of nonmarket R&D used by the economy as a whole is of importance.

Conclusions from the exercise (contd. ) • The treatment of non-market R&D in this way is consistent with the treatment of roads and other infrastructure in the current SNA. • However, it is important to show such R&D separately, since it is used by other sectors. • Although the individual use mostly can not be identified, the scope of nonmarket R&D used by the economy as a whole is of importance.

• The compilation of bridge tables and R&D") Conclusions from the exercise (contd. ) • The compilation of bridge tables and R&D capitalization process would very likely lead to an improvement of R&D estimates in the national accounts. • Improvement seems to be necessary, whether R&D is capitalized or not. There is a need for separate R&D accounts of a good quality in the SNA framework for economic analysis's and decisions.

Conclusions from the exercise (contd. ) • The compilation of bridge tables and R&D capitalization process would very likely lead to an improvement of R&D estimates in the national accounts. • Improvement seems to be necessary, whether R&D is capitalized or not. There is a need for separate R&D accounts of a good quality in the SNA framework for economic analysis's and decisions.