4678ce871dc3327cd56a785f83f6dd4b.ppt

- Количество слайдов: 47

Board Governance Efficiency through OCIO Leading Age North Carolina May 2017 This report has been prepared by UBS Financial Services Inc. (UBS FS). Please see important disclaimers and disclosures beginning at the end of this document.

Governance

Trends in Board Governance • Sarbanes-Oxley Act never formally extended to non-profits but its provisions have altered expectoration and standards about non-profit governance. • Non- Profit Boards face an increasingly difficult regulatory environment. • Board sophistication and accountability. Successful boards know that simply having a strategic plan is not enough. It is the Board's duty to see that the plan is being effectively executed. • Focus on mission and implementation of strategic plans. Boards need to resist the danger of becoming too enmeshed in daily operations. 2

,")

Outsourced OCIO? • The term “outsourced CIO, ” or “outsourced chief investment officer” (“OCIO”), is shorthand for describing an arrangement through which those responsible for managing the organization’s long-term monies delegate investment responsibility to a third party. • A board or an investment committee may seek to enter into such an arrangement because its members may not have extensive investment experience themselves, lack the time to manage it themselves or with a traditional consultant, or because they seek access to a more sophisticated asset allocation strategy. • An institution seeking new ways to meet its capital and growth needs may wish to consider an OCIO arrangement. Source: UBS publication Insights for Fiduciaries - "Outsourced CIO "– fiduciary issues and considerations for foundations and endowments. 3

OCIO Supports Fiduciary Responsibilities Challenges Discretionary Solution • Preparing a prudent Investment Policy Statement (IPS) including the proper target asset allocation. • Consultant will help you determine an appropriate asset allocation and investment strategy for your organization’s portfolio. • Diversifying investment assets to fit your specific risk/return profile. • Portfolio composed of solutions from investment management organizations that have expertise and skills in their respective asset classes and styles. • Selecting and monitoring investment managers/funds using a robust due diligence process. • Consultant employs a disciplined process for investment manager/fund selection and portfolio construction based on qualitative and quantitative research and analysis. • Understanding of the investment risks and if you are achieving your objectives. • Consultant monitors risk exposure, reports on progress towards investment objectives and rebalance as needed. • Lack of expertise or resources to meet the investment objectives and conduct ongoing oversight. • Services include assistance with Investment Policy Statement development, asset allocation implementation based on your IPS, selection and monitoring of investment strategies and funds, performance reporting. 4

Policy and Discretion

identifies a target asset allocation aligned")

Determining your objectives The Investment Policy Statement (IPS) identifies a target asset allocation aligned with your organization’s return objective, risk tolerance, time horizon and other relevant investment considerations. YOUR COMPANY Investment Policy Statement Version 1. 0 6

Asset allocation & Spending policy analysis • Takes a strategic approach to asset allocation that uses quantitative portfolio optimization technology to define the efficient frontier. • Provides a disciplined approach to assembling portfolios that are designed to provide a potential return for a given level of quantifiable risk • Should be reviewed periodically to adjust to changes in capital market expectations, the actual returns experienced by the underlying investments and/or changes in the objectives of the fund • Should analyze your liabilities against your assets and recommend a Spending Policy commensurate with your cash flow requirements, initially and on an ongoing basis. Asset Allocation Development Annual Spending as a % of Assets Index Spending to an Inflation Rate A % of Assets for a Rolling Time Frame 7

Asset Allocation

Asset Allocation: Forward-looking & Historical Risk/Return Statistics Proposed Non- Traditional, 20% U. S. Equity, 40% Non-U. S. Fixed Income, 3% U. S. Fixed Income, 22% Non-U. S. Equity, 15% Proposed Forward-Looking Data Estimated Return Estimated Standard Deviation Estimated Sharpe Ratio 7. 04% 12. 75% 0. 36 Historical Data (5 Years Ending 6/30/2016) Annualized Return Annualized Standard Deviation Sharpe Ratio Best Rolling Year Worst Rolling Year 6. 73% 9. 35% 0. 71 19. 96% (05/2012 - 05/2013) -8. 41% (02/2015 - 02/2016) The information provided to you is for informational purposes only and it should not be regarded as an offer to sell or as a solicitation of an offer to buy any securities. Results shown are hypothetical, are provided for illustrative purposes only and do not include the impact of transaction costs, taxes and inflation. If included, the results shown would be lower. The results are based on UBS simulation over the specified time horizon. Actual results may vary depending on the specific composition of the investor's portfolio. Actual results may also vary depending on when the portfolio is implemented and may be affected by changing market conditions. Past performance or historic results provide no guarantee of future returns. Forward-looking estimated results and probabilistic analysis should not be construed as a guarantee and are provided for illustrative purposes only. See Appendix A: Important Information You Should Know

Asset Allocation: Portfolio In Detail & Estimated Cash Flows Asset Class Cash Fixed Income U. S. Taxable Core Multisector Fund Investment Grade Corporates High Yield Corporates Non-U. S. Fixed Income Developed Fixed Income Equity U. S. Equity Large-Cap Core Large-Cap Growth Large-Cap Value SMID-Cap Growth SMID-Cap Value Non-U. S. Equity Developed Equity Emerging Equity Non-Traditional Hedge Funds Credit Strategies Equity Hedge Private Equity (PE) Private Real Estate Private RE Total Asset Class Benchmark Barclays 1 -3 Month Treasury Bill Barclays U. S. Aggregate - Investment Grade Barclays U. S. Aggregate - High Yield Proposed Asset Allocation Est. Yield Est. Cash Allocation $ Flow % % $ 0. 0% 25. 0% 23. 0% 4. 0% 3. 0% 12. 0% 4. 0% 2. 0% Barclays Global Aggregate x. US 2. 0% 55. 0% 40. 0% $0 0. 12% $32, 500, 000 3. 97% $29, 900, 000 4. 22% $0 $1, 289, 990 $1, 262, 690 $5, 200, 000 $3, 900, 000 $15, 600, 000 $5, 200, 000 2. 59% 3. 67% 8. 74% $134, 680 $101, 010 $572, 520 $454, 480 $2, 600, 000 1. 05% $27, 300 $71, 500, 000 $52, 000 2. 24% 1. 99% $1, 599, 471 $1, 036, 310 $13, 000 $11, 700, 000 $7, 800, 000 2. 21% 1. 47% 2. 68% 1. 04% 2. 34% $287, 476 $171, 714 $313, 372 $80, 896 $182, 852 S&P 500 Russell 1000 Growth Russell 1000 Value Russell 2500 Growth Russell 2500 Value 10. 0% 9. 0% 6. 0% 15. 0% $19, 500, 000 2. 89% $563, 161 MSCI EAFE MSCI Emerging Markets 10. 0% 5. 0% $13, 000 $6, 500, 000 2. 96% 2. 74% $384, 939 $178, 222 $26, 000 $13, 000 0. 00% $0 $0 5. 0% $6, 500, 000 0. 00% $0 $0 $130, 000 2. 22% 20. 0% 10. 0% HFRI Distressed & Restructuring HFRI Equity Hedge LPX America NCREIF 100. 0% $2, 889, 461 Estimated Yield and Cash flow are based on index data. The information provided to you is for informational purposes only and it should not be regarded as an offer to sell or as a solicitation of an offer to buy any securities. Results shown are hypothetical, are provided for illustrative purposes only and do not include the impact of transaction costs, taxes and inflation. If included, the results shown would be lower. Actual results may vary depending on the specific composition of the investor's portfolio. Actual results may also vary depending on when the portfolio is implemented and may be affected by changing market conditions. .

Asset Allocation: Monte Carlo Simulations Simulated historic and probabilistic analysis Proposed The graph shows the historical development of the asset allocation and the resulting value percentiles of the Monte. Carlo simulation. 1, 200, 000 For example: The 50 th percentile line indicates the value which will be exceeded in 50 % of the cases. IMPORTANT: The projections or other information shown regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results and are not guarantees of future results. 1, 073, 886, 189 1, 000, 000 USD ($) 800, 000, 000 629, 976, 96 3 400, 000 440, 557, 67 2 296, 158, 97 4 200, 000 166, 489, 70 1 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 0 History 5 th%ile 25 th%ile 50 th%ile 75 th%ile 95 th%ile Data as of 6/30/2016 The information provided to you is for informational purposes only and it should not be regarded as an offer to sell or as a solicitation of an offer to buy any securities. Results shown are hypothetical, are provided for illustrative purposes only and do not include the impact of transaction costs, taxes and inflation. If included, the results shown would be lower. The results are based on UBS simulation over the specified time horizon. Actual results may vary depending on the specific composition of the investor's portfolio. Actual results may also vary depending on when the portfolio is implemented and may be affected by changing market conditions. Past performance or historic results provide no guarantee of future returns. Forward-looking estimated results and probabilistic analysis should not be construed as a guarantee and are provided for illustrative purposes only. See Appendix A: Important Information You Should Know for details.

Asset Allocation: Summary of Simulations Performed Simulation with Forward Looking Risk Model over 20 years Probability of Being Below Stated Value Portfolio (current value $130, 000) Proposed 5% 25% 50% 75% 95% 166, 489, 701 296, 158, 974 440, 557, 672 629, 976, 963 1, 073, 886, 189 25% 4. 20% 50% 6. 29% 75% 8. 21% 95% 11. 13% Probability of Being Below Stated Annualized Returns Portfolio 5% Proposed 1. 24% Data as of 6/30/2016 The information provided to you is for informational purposes only and it should not be regarded as an offer to sell or as a solicitation of an offer to buy any securities. Results shown are hypothetical, are provided for illustrative purposes only and do not include the impact of transaction costs, taxes and inflation. If included, the results shown would be lower. The results are based on UBS simulation over the specified time horizon. Actual results may vary depending on the specific composition of the investor's portfolio. Actual results may also vary depending on when the portfolio is implemented and may be affected by changing market conditions. Past performance or historic results provide no guarantee of future returns. Forward-looking estimated results and probabilistic analysis should not be construed as a guarantee and are provided for illustrative purposes only. See Appendix A: Important Information You Should Know for details.

Asset Allocation: Historical Analysis and Efficient Frontier Simulated Historical performance Test Simulated Historical Stress 200 5. 00 180 0. 00 160 -5. 00 140 -10. 00 Returns (%) 120 US D 100 80 -15. 00 -20. 00 -25. 00 60 40 -30. 00 20 -35. 00 2006 0 2008 2012 2015 2007 2011 2009 2013 2016 -40. 00 2014 Proposed Simulated Historical Annual Returns Tech Bubble '00/01 -9. 31 Sept 11 '01 2 nd Gulf War '03 -14. 39 -8. 80 Recession '02 1. 13 Credit Crunch '08/09 -37. 87 Political Crisis '11 -12. 76 Forward-Looking Efficient Frontier 40. 00 12. 00% 30. 00 10. 00% 20. 00 Annualized Estimated Return 8. 00% Returns (%) 10. 00 6. 00% 0. 00 4. 00% -10. 00 2. 00% -20. 00 -30. 00% 5. 00% 10. 00% 15. 00% 20. 00% 25. 00% 30. 00% Annualized Estimated Risk -40. 00 Proposed 2007 2008 2009 2010 2011 2012 2013 2014 2015 YTD 2016 6. 98 -30. 58 28. 50 15. 89 -0. 34 14. 57 18. 44 5. 52 -1. 63 3. 90 Proposed Data as of 6/30/2016 The information provided to you is for informational purposes only and it should not be regarded as an offer to sell or as a solicitation of an offer to buy any securities. Results shown are hypothetical, are provided for illustrative purposes only and do not include the impact of transaction costs, taxes and inflation. If included, the results shown would be lower. The results are based on UBS simulation over the specified time horizon. Actual results may vary depending on the specific composition of the investor's portfolio. Actual results may also vary depending on when the portfolio is implemented and may be affected by changing market conditions. Past performance or historic results provide no guarantee of future returns. Forward-looking estimated results and probabilistic analysis should not be construed as a guarantee and are provided for illustrative purposes only. See Appendix A: Important Information You Should Know for details.

Asset Allocation: Rolling 1 - and 3 -Year Risk 1 -Year Rolling Risk These charts show historic risk , or volatility, over rolling 1 - and 3 -year periods. On a 1 -Year rolling basis, portfolios are subject to increased risk as there isn't sufficient time to withstand periods of market instability. 30. 00 However when viewed over longer time horizons, portfolio returns tend to revert to their mean, helping to reduce overall risk by mitigating periods with higher volatility. 25. 00 20. 00 Risk (%) 15. 00 10. 00 5. 00 0. 00 Proposed 3 -Years Rolling Risk 30. 00 25. 00 20. 00 Risk (%) 15. 00 10. 00 5. 00 0. 00 Proposed Rolling monthly performances from 8/31/2003 through 6/30/2016 The information provided to you is for informational purposes only and it should not be regarded as an offer to sell or as a solicitation of an offer to buy any securities. Results shown are hypothetical, are provided for illustrative purposes only and do not include the impact of transaction costs, taxes and inflation. If included, the results shown would be lower. The results are based on UBS simulation over the specified time horizon. Actual results may vary depending on the specific composition of the investor's portfolio. Actual results may also vary depending on when the portfolio is implemented and may be affected by changing market conditions. Past performance or historic results provide no guarantee of future returns. Forward-looking estimated results and probabilistic analysis should not be construed as a guarantee and are provided for illustrative purposes only. See for details. Appendix A: Important Information You Should Know

Returns Risk Proposed Risk")

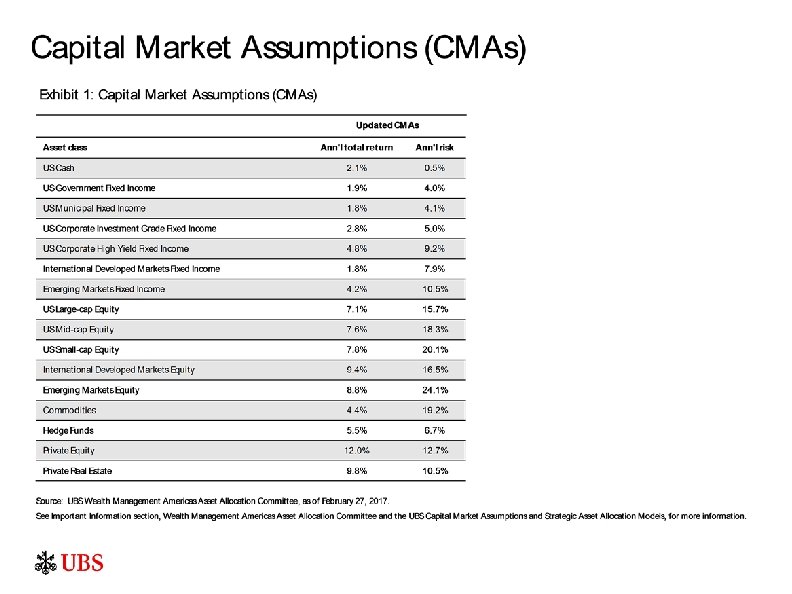

Asset Allocation: Risk Contribution UBS WMA's Capital Market Assumption (CMAs) Returns Risk Proposed Risk Weight Contribution 25. 0% US Fixed Income 6. 6% 21. 8% Fixed Income 5. 6% US Fixed Core 2. 7% 3. 5% 4. 0% 0. 1% US Government 2. 2% 4. 3% 0. 6% -0. 1% US Credit 3. 5% 5. 9% 13. 2% 2. 6% US High Yield 5. 6% 11. 7% 4. 0% 2. 9% 3. 2% 1. 0% Non-US Fixed Income Global FI ex US 4. 0% 9. 0% 3. 2% 1. 0% 55. 0% Equity 78. 4% 40. 0% 54. 4% Large-Cap Core 7. 5% 16. 8% 10. 0% 12. 8% Large-Cap Growth 7. 4% 16. 8% 9. 0% 11. 4% Large-Cap Value 7. 6% 17. 4% 9. 0% 11. 7% SMID-Cap 8. 5% 20. 7% 12. 0% 18. 5% 15. 0% 23. 9% US Equity Non-US Equity Ex-US Developed Emerging 8. 5% 19. 7% 10. 0% 14. 8% 10. 0% 25. 5% 5. 0% 9. 1% 20. 0% 15. 0% Non-Traditional 10. 0% 5. 6% Equity Hedge 6. 2% 9. 4% 5. 0% 3. 4% Credit Strategies 6. 2% 6. 7% 5. 0% 2. 2% 11. 8% 24. 4% 5. 0% 8. 2% 8. 5% 11. 8% 5. 0% Hedge Funds PE Private RE Total Portfolio Risk: 1. 2% 12. 8% Data as of 6/30/2016 for details. The information provided to you is for informational purposes only and it should not be regarded as an offer to sell or as a solicitation of an offer to buy any securities. Results shown are hypothetical, are provided for illustrative purposes only and do not include the impact of transaction costs, taxes and inflation. If included, the results shown would be lower. The results are based on UBS simulation over the specified time horizon. Actual results may vary depending on the specific composition of the investor's portfolio. Actual results may also vary depending on when the portfolio is implemented and may be affected by changing market conditions. Past performance or historic results provide no guarantee of future returns. Forward-looking estimated results and probabilistic analysis should not be construed as a guarantee and are provided for illustrative purposes only. See Appendix A: Important Information You Should Know

Setting the stage

What has happened recently? Markets continue to make new gains amid political uncertainty Source: Bloomberg, UBS, as of 26 April 2017. 18

How have asset classes performed? Moderate diversified portfolios are up over 5% year to date, following a 5% return in 2016 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 Highest 66. 5% return 13. 2% 7. 2% 11. 5% 55. 8% 25. 6% 34. 0% 32. 1% 39. 4% 12. 4% 78. 5% 26. 9% 10. 7% 18. 2% 38. 8% 13. 2% 3. 3% 21. 3% 14. 1% 27. 0% 11. 7% 5. 3% 9. 6% 47. 3% 20. 3% 13. 5% 26. 3% 11. 2% -2. 5% 58. 2% 18. 9% 9. 0% 17. 3% 33. 1% 9. 1% 0. 9% 17. 1% 10. 1% 21. 3% 0. 2% 5. 1% -4. 2% 38. 6% 18. 3% 8. 0% 18. 4% 8. 7% -21. 8% 31. 8% 16. 1% 5. 0% 16. 4% 22. 8% 6. 4% 0. 9% 12. 1% 7. 4% 20. 9% -3. 0% 2. 5% -1. 4% 29. 9% 11. 4% 6. 3% 15. 5% 7. 3% -26. 2% 28. 4% 15. 1% 1. 8% 16. 3% 11. 8% 4. 9% 0. 1% 11. 2% 5. 5% 13. 5% -5. 9% -2. 6% -6. 2% 29. 0% 11. 1% 4. 6% 13. 0% 5. 8% -33. 8% 27. 2% 9. 2% 1. 5% 15. 8% 7. 4% 4. 9% -0. 8% 5. 2% 4. 8% 2. 4% -7. 8% -3. 6% -15. 9% 21. 9% 10. 8% 3. 5% 11. 8% 3. 4% -37. 6% 24. 8% 7. 8% -4. 2% 11. 7% -2. 6% 2. 5% -4. 4% 1. 0% 3. 7% -2. 1% -14. 2% -12. 4% -20. 5% 5. 3% 4. 5% 2. 7% 4. 8% 1. 9% -43. 4% 12. 9% 5. 5% -12. 1% 6. 8% -2. 6% -2. 2% -4. 5% 1. 0% 2. 3% Lowest -2. 2% return -30. 8% -21. 4% -21. 7% 2. 4% 3. 5% 2. 7% 3. 5% -1. 6% -53. 3% -2. 2% 2. 4% -18. 4% 2. 0% -2. 6% -4. 9% -14. 9% 0. 2% 1. 3% Source: Bloomberg, UBS, as of 27 April 2017 Note: The Moderate Diversified Portfolio performance calculations are based on the current Strategic Asset Allocation (SAA) for a moderate risk profile investor in a taxable portfolio without non-traditional assets. It doesn't take into account any prior SAA for this investor profile and includes time periods before the SAA was created. See the latest UBS House View: Investment Strategy Guide (ISG) for the detailed SAA of the taxable portfolio without non-traditional assets. The performance calculations reflect an annual rebalancing. These calculations will not match the performance measurement published in the ISG, which reflects a monthly rebalancing. For periods prior to 2009, this illustration assumes that the Bloomberg Barclays EM Local Currency Government Total Return Index allocation (inception date of 4 July 2008) was invested fully in the Bloomberg Barclays EM USD Aggregate Total Return Index. 19

What are the key market risks? Likelihood of key market risks across the globe Source: UBS, as of 26 April 2017. Note: The CIO risk score is a composite of four risk "dimensions: " probability (the likelihood of occurrence within the next 6 -12 months), urgency (how soon the event would likely take place), geographic scope (the extent of regional/global financial and economic contagion), and expected market impact (by how much the returns on the affected asset classes would deviate from the baseline). Each dimension score can take a value between 1 and 4, with 4 being the highest risk level; the overall CIO risk score is the average of the scores for the four risk dimensions. 20

2017 will see another round of political risk Stacked 2017 political calendar % of votes won in national election – January: US presidential inauguration 40% – March: Dutch general election 30% – April: French presidential election round 1 20% – May: French presidential election round 2 – October: German federal election Anti-establishment parties gaining popularity in Europe. 10% 0% 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 Freedom Party (Austria) Front national (France) Syriza (Greece) Podemos (Spain) Danish People's Party (Denmark) Five star movement (Italy) Swedish Democrats (Sweden) Af. D (Germany) Finns Party / True Finns (Finland) UKIP (UK) The end game? Interactive feature on ubs. com/cio Play policymaker – tackle the world's economic problems Understand the implications of policy decisions on economies, markets, and portfolios. Source: National elections; UBS House View January 2017 21

Economy at a glance

Core message Global economic data continues to advance, pointing to a simultaneous acceleration for the US, Eurozone, and emerging markets Economic growth is already poised to speed up due to fading headwinds, and potential fiscal stimulus from a Trump presidency could further add to growth and inflation improvements Monetary policy continues to normalize, but remains supportive We continue to recommend an overweight to global and US large-cap stocks Within fixed income, we prefer high yield corporate bonds over standard government bonds 23

Core message What is currently happening? Markets have weathered political volatility Central bank rates remain near historic lows US PMIs consistent with moderate growth ISM Purchasing Managers Indices 60 55 50 Markets have focused on pro-growth policies in the aftermath of the US election 45 40 35 Growth and inflation expectations have picked up, spurring higher bond yields 30 2008 2009 2010 2011 Composite PMI 2012 2013 2014 2015 2016 Manufacturing PMI 2017 Non-manufacturing PMI Source: Bloomberg, UBS, as of 27 April 2017 24

Markets have weathered political volatility… After initial volatility, markets have recovered quickly from shocks Global and US large-cap stocks since the end of 2015 Source: Bloomberg, UBS, as of 26 April 2017 25

Global interest rates remain near historic lows Central bank policy remains easy, with few prospects for rate hikes outside the US Policy rate (%) with UBS forecast 6 5 4 3 2 1 0 -1 2008 2009 2010 2011 US 2012 UK 2013 2014 2015 Switzerland Euro area 2016 Japan 2017 2018 2019 Source: Bloomberg, UBS, as of 26 April 2017 26

Consumer and business confidence has jumped… Largest jump in small-business optimism since 1980 • Tax reform • Regulatory relief • Infrastructure spending plan Source: Bloomberg, UBS, as of 26 April 2017 27

…despite policy uncertainty and potential risks Policy uncertainty remains elevated US Economic Policy Uncertainty Index (news-based) Election Day 160 140 120 • Trade policy 100 • Immigration reform 80 • Global engagement 60 40 Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Source: Bloomberg, UBS, as of 26 April 2017 28

…and anticipating increased growth and inflation Stimulus hopes have boosted inflation expectations… …and accelerated the anticipated pace of rate hikes Fed funds futures yields 2. 8% 2. 00% 2. 5% 1. 75% 2. 3% 2. 0% >24 Months (May 18) 1. 25% 1. 8% 25 Months (Sep 19 -> Aug 17) 1. 00% 1. 5% 15 Months (Jun 18 -> Mar 17) 0. 75% 1. 3% 1. 0% 06 -2015 >24 Months (Feb 19) 1. 50% 0. 50% 12 -2015 06 -2016 12 -2016 10 -year Treasury yield (rhs) 10 -year inflation breakeven 0. 25% 11/2016 11/2017 11/8/2016 11/2018 11/2019 4/26/2017 Source: Bloomberg, UBS, as of 26 April 2017 29

Potential fiscal stimulus could boost GDP… Trump's fiscal policies could add as much as 0. 5% to growth, but fading headwinds are the main drivers UBS US economic forecast (real GDP) Potential fiscal stimulus (estimate) Source: UBS, as of 26 April 2017 30

…and bolster earnings growth acceleration Fiscal stimulus measures could add a further 3– 13% over the next few years. UBS S&P 500 earnings per share estimates, in USD Potential fiscal stimulus (estimates) 145 132. 5 119 118 119 2014 2015 2016 110 104 98 2011 2012 2013 2017 F 2018 F Source: UBS, as of 26 April 2017 31

Looking ahead What will and won't happen?

Core message What will happen? US and global growth will accelerate moderately Global economic growth is accelerating, despite slower growth in some areas Real GDP, actual and UBS forecasts 8% US earnings growth will continue to accelerate 7% 6% 5% Central banks will continue to provide liquidity 4% 3% 2% The Fed will continue to raise rates 1% 0% US Eurozone 2016 F Source: Bloomberg, UBS, as of 26 April 2017 UK 2017 F Japan China World* 2018 F * Excludes Venezuela 33

US earnings will continue to accelerate Earnings growth is rebounding Consensus S&P 500 (total and ex-Energy) EPS growth, in % y/y Source: Bloomberg, UBS, as of 26 April 2017 34

Central banks will continue to provide liquidity Balance sheets have been boosted by quantitative easing Central bank balance sheets (in USD trillions) 600 500 400 300 200 100 0 2006 2007 2008 Fed 2009 ECB 2010 2011 Bank of Japan 2012 2013 2014 2015 2016 Bank of China Source: Bloomberg, UBS, as of 26 April 2017 35

The Fed will continue to raise rates The market now expects several additional rate hikes through the end of 2019 Fed funds futures, yield in % 2. 00% 1. 75% 1. 50% 1. 25% 1. 00% 0. 75% 0. 50% 0. 25% 0. 00% 11/2016 05/2017 11/2017 05/2018 11/8/2016 11/2018 05/2019 11/2019 05/2020 4/26/2017 Source: Bloomberg, UBS, as of 26 April 2017. 36

Core message What won't happen? US will not face a recession Key indicators still show economic health Conference Board US Leading Index (10 indicators) 130 China will not face a hard landing 120 A bear market will not begin in the US 110 100 90 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 Recession indicator Conference board Index Source: Bloomberg, UBS, as of 26 April 2017 37

China will not face an economic hard landing Chinese policy should remain accommodative Bank of China balance sheet, in CNY billions Chinese growth should gradually moderate China GDP, actual and UBS forecast, in % 40, 000 9 35, 000 8 30, 000 7 6 25, 000 5 20, 000 4 15, 000 3 10, 000 2 5, 000 0 2005 1 0 2009 2013 2017 2013 2014 2015 2016 2017 F 2018 F Source: Bloomberg, UBS, as of 26 April 2017 38

A bear market will not begin in the US The bull market has continued despite multiple instances of increased volatility S&P 500 and VIX index throughout the current bull market S&P 500 2600 15 Oct 2014: -7. 4% 2200 1800 24 June 2013: -5. 8% 1 Jun 2012: -9. 9% 3 Oct 2011: -19. 4% 25 Aug 2015: -12. 4% 11 Feb 2016: -13. 3% 1400 1000 2011 VIX 60 2012 2013 2014 2015 2016 2017 50 40 30 20 10 0 2011 Source: Bloomberg, UBS, as of 26 April 2017 39

Appendix: Investment committees Global Investment Process and Committee Description The UBS investment process is designed to achieve replicable, high quality results through applying intellectual rigor, strong process governance, clear responsibility and a culture of challenge. Based on the analyses and assessments conducted and vetted throughout the investment process, the Chief Investment Officer (CIO) formulates the UBS Wealth Management Investment House View (e. g. , overweight, neutral, underweight stance for asset classes and market segments relative to their benchmark allocation) at the Global Investment Committee (GIC). Senior investment professionals from across UBS, complemented by selected external experts, debate and rigorously challenge the investment strategy to ensure consistency and risk control. Global Investment Committee Composition The GIC is comprised of 10 members, representing top market and investment expertise from across all divisions of UBS: • Mark Haefele (Chair) • Mark Andersen • Jorge Mariscal • Mike Ryan • Simon Smiles • Tan Min Lan • Themistocleous • Paul Donovan • Bruno Marxer (*) • Andreas Koester (*) Business areas distinct from Chief Investment Office/Wealth Management Research WMA Asset Allocation Committee Description We recognize that a globally derived house view is most effective when complemented by local perspective and application. As such, UBS has formed a Wealth Management Americas Asset Allocation Committee (WMA AAC). WMA AAC is responsible for the development and monitoring of UBS WMA’s strategic asset allocation models and capital market assumptions. The WMA AAC sets parameters for the CIO WMR Americas Investment Strategy Group to follow during the translation process of the GIC’s House Views and the incorporation of US-specific asset class views into the US-specific tactical asset allocation models. WMA Asset Allocation Committee Composition The WMA Asset Allocation Committee is comprised of five members: • Mike Ryan • Michael Crook • Richard Hollmann (*) • Brian Rose • Jeremy Zirin (*) Business areas distinct from Chief Investment Office/Wealth Management Research 40

Appendix: Statement of risk 1. Equity markets are difficult to forecast because of fluctuations in the economy, investor psychology, geopolitical conditions, and other important variables. 2. Bond market returns are difficult to forecast because of fluctuations in the economy, investor psychology, geopolitical conditions and other important variables. Corporate bonds are subject to a number of risks, including credit risk, interest rate risk, liquidity risk, and event risk. Though historical default rates are low on investment grade corporate bonds, perceived adverse changes in the credit quality of an issuer may negatively affect the market value of securities. As interest rates rise, the value of a fixed coupon security will likely decline. Bonds are subject to market value fluctuations, given changes in the level of risk-free interest rates. Not all bonds can be sold quickly or easily on the open market. Prospective investors should consult their tax advisors concerning the federal, state, local, and non-U. S. tax consequences of owning any securities referenced in this report. 3. Prospective investors should consult their tax advisors concerning the federal, state, local, and non-U. S. tax consequences of owning preferred stocks. Preferred stocks are subject to market value fluctuations, given changes in the level of interest rates. For example, if interest rates rise, the value of these securities could decline. If preferred stocks are sold prior to maturity, price and yield may vary. Adverse changes in the credit quality of the issuer may negatively affect the market value of the securities. Most preferred securities may be redeemed at par after five years. If this occurs, holders of the securities may be faced with a reinvestment decision at lower future rates. Preferred stocks are also subject to other risks, including illiquidity and certain special redemption provisions. 4. Although historical default rates are very low, all municipal bonds carry credit risk, with the degree of risk largely following the particular bond’s sector. Additionally, all municipal bonds feature valuation, return, and liquidity risk. Valuation tends to follow internal and external factors, including the level of interest rates, bond ratings, supply factors, and media reporting. These can be difficult or impossible to project accurately. Also, most municipal bonds are callable and/or subject to earlier than expected redemption, which can reduce an investor’s total return. Because of the large number of municipal issuers and credit structures, not all bonds can be easily or quickly sold on the open market. End Notes “CIO WMR tactical deviation” legend: Overweight Underweight Neutral Source: UBS and WMA AAC, 20 April 2017. See appendix for information regarding sources of strategic asset allocations and their suitability, investor risk profiles, and the interpretation of the suggested tactical deviations from the strategic asset allocations. Change legend: ▲ Upgrade ▼ Downgrade, refers to moderate-risk profile 1 Change is the difference between the tactical deviation column in the previous month and the current month. 2 The current allocation column is the sum of the strategic asset allocation and the tactical deviation columns. 3 The Bloomberg Barclays US Treasury Bellwethers 10 Year Total Return Index is used as the benchmark for US government 10 -year bonds. 4 The MSCI All Country World Index is used as the benchmark for global equity. 41

Appendix Emerging Market Investments Investors should be aware that Emerging Market assets are subject to, amongst others, potential risks linked to currency volatility, abrupt changes in the cost of capital and the economic growth outlook, as well as regulatory and socio-political risk, interest rate risk and higher credit risk. Assets can sometimes be very illiquid and liquidity conditions can abruptly worsen. WMR generally recommends only those securities it believes have been registered under Federal U. S. registration rules (Section 12 of the Securities Exchange Act of 1934) and individual State registration rules (commonly known as "Blue Sky" laws). Prospective investors should be aware that to the extent permitted under US law, WMR may from time to time recommend bonds that are not registered under US or State securities laws. These bonds may be issued in jurisdictions where the level of required disclosures to be made by issuers is not as frequent or complete as that required by US laws. For more background on emerging markets generally, see the WMR Education Notes "Investing in Emerging Markets (Part 1): Equities", 27 August 2007, "Emerging Market Bonds: Understanding Emerging Market Bonds, " 12 August 2009 and "Emerging Markets Bonds: Understanding Sovereign Risk, " 17 December 2009. Investors interested in holding bonds for a longer period are advised to select the bonds of those sovereigns with the highest credit ratings (in the investment grade band). Such an approach should decrease the risk that an investor could end up holding bonds on which the sovereign has defaulted. Sub-investment grade bonds are recommended only for clients with a higher risk tolerance and who seek to hold higher yielding bonds for shorter periods only. Non-Traditional Assets Non-traditional asset classes are alternative investments that include hedge funds, private equity, real estate, and managed futures (collectively, alternative investments). Interests of alternative investment funds are sold only to qualified investors, and only by means of offering documents that include information about the risks, performance and expenses of alternative investment funds, and which clients are urged to read carefully before subscribing and retain. An investment in an alternative investment fund is speculative and involves significant risks. Specifically, these investments (1) are not mutual funds and are not subject to the same regulatory requirements as mutual funds; (2) may have performance that is volatile, and investors may lose all or a substantial amount of their investment; (3) may engage in leverage and other speculative investment practices that may increase the risk of investment loss; (4) are long-term, illiquid investments, there is generally no secondary market for the interests of a fund, and none is expected to develop; (5) interests of alternative investment funds typically will be illiquid and subject to restrictions on transfer; (6) may not be required to provide periodic pricing or valuation information to investors; (7) generally involve complex tax strategies and there may be delays in distributing tax information to investors; (8) are subject to high fees, including management fees and other fees and expenses, all of which will reduce profits. Interests in alternative investment funds are not deposits or obligations of, or guaranteed or endorsed by, any bank or other insured depository institution, and are not federally insured by the Federal Deposit Insurance Corporation, the Federal Reserve Board, or any other governmental agency. Prospective investors should understand these risks and have the financial ability and willingness to accept them for an extended period of time before making an investment in an alternative investment fund and should consider an alternative investment fund as a supplement to an overall investment program. In addition to the risks that apply to alternative investments generally, the following are additional risks related to an investment in these strategies: Hedge Fund Risk: There are risks specifically associated with investing in hedge funds, which may include risks associated with investing in short sales, options, small-cap stocks, "junk bonds, " derivatives, distressed securities, non-U. S. securities and illiquid investments. Managed Futures: There are risks specifically associated with investing in managed futures programs. For example, not all managers focus on all strategies at all times, and managed futures strategies may have material directional elements. Real Estate: There are risks specifically associated with investing in real estate products and real estate investment trusts. They involve risks associated with debt, adverse changes in general economic or local market conditions, changes in governmental, tax, real estate and zoning laws or regulations, risks associated with capital calls and, for some real estate products, the risks associated with the ability to qualify for favorable treatment under the federal tax laws. Private Equity: There are risks specifically associated with investing in private equity. Capital calls can be made on short no-tice, and the failure to meet capital calls can result in significant adverse consequences including, but not limited to, a total loss of investment. Foreign Exchange/Currency Risk: Investors in securities of issuers located outside of the United States should be aware that even for securities denominated in U. S. dollars, changes in the exchange rate between the U. S. dollar and the issuer’s "home" currency can have unexpected effects on the market value and liquidity of those securities. Those securities may also be affected by other risks (such as political, economic or regulatory changes) that may not be readily known to a U. S. investor. 42

Appendix: explanations about asset allocations Sources of strategic asset allocations and investor risk profiles Strategic asset allocations represent the longer-term allocation of assets that is deemed suitable for a particular investor. The strategic asset allocation models discussed in this publication, and the capital market assumptions used for the strategic asset allocations, were developed and approved by the WMA AAC. The strategic asset allocations are provided for illustrative purposes only and were designed by the WMA AAC for hypothetical US investors with a total return objective under five different Investor Risk Profiles ranging from conservative to aggressive. In general, strategic asset allocations will differ among investors according to their individual circumstances, risk tolerance, return objectives and time horizon. Therefore, the strategic asset allocations in this publication may not be suitable for all investors or investment goals and should not be used as the sole basis of any investment decision. Minimum net worth requirements may apply to allocations to non-traditional assets. As always, please consult your UBS Financial Advisor to see how these weightings should be applied or modified according to your individual profile and investment goals. The process by which the strategic asset allocations were derived is described in detail in the publication entitled “Strategic Asset Allocation (SAA) Methodology and Portfolios, ” published on 26 February 2017. Your Financial Advisor can provide you with a opy. c Deviations from strategic asset allocation or benchmark allocation The recommended tactical deviations from the strategic asset allocation or benchmark allocation are provided by the Global Investment Committee and the Investment Strategy Group within CIO Wealth Management Research Americas. They reflect the short- to medium-term assessment of market opportunities and risks in the respective asset classes and market segments. Positive/zero/negative tactical deviations correspond to an overweight/neutral/underweight stance for each respective asset class and market segment relative to their strategic allocation. The current allocation is the sum of the strategic asset allocation and the tactical deviation. Note that the regional allocations on the Equities and Bonds pages in UBS House View are provided on an unhedged basis (i. e. , it is assumed that investors carry the underlying currency risk of such investments) unless otherwise stated. Thus, the deviations from the strategic asset allocation reflect the views of the underlying equity and bond markets in combination with the assessment of the associated currencies. The detailed asset allocation tables integrate the country preferences within each asset class with the asset class preferences in UBS House View. Asset allocation does not assure profits or prevent against losses from an investment portfolio or accounts in a declining arket. m NOTE: TACTICAL TIME HORIZON IS APPROXIMATELY SIX MONTHS 43

Wealth Management (WM) Research is published by UBS")

Appendix: Disclaimer Chief Investment Office (CIO) Wealth Management (WM) Research is published by UBS Wealth Management and UBS Wealth Management Americas, Business Divisions of UBS AG (UBS) or an affiliate thereof. CIO WM Research reports published outside the US are branded as Chief Investment Office WM. In certain countries UBS AG is referred to as UBS SA. This publication is for your information only and is not intended as an offer, or a solicitation of an offer, to buy or sell any investment or other specific product. The analysis contained herein does not constitute a personal recommendation or take into account the particular investment objectives, investment strategies, financial situation and needs of any specific recipient. It is based on numerous assumptions. Different assumptions could result in materially different results. We recommend that you obtain financial and/or tax advice as to the implications (including tax) of investing in the manner described or in any of the products mentioned herein. Certain services and products are subject to legal restrictions and cannot be offered worldwide on an unrestricted basis and/or may not be eligible for sale to all investors. All information and opinions expressed in this document were obtained from sources believed to be reliable and in good faith, but no representation or warranty, express or implied, is made as to its accuracy or completeness (other than disclosures relating to UBS and its affiliates). All information and opinions as well as any prices indicated are current only as of the date of this report, and are subject to change without notice. Opinions expressed herein may differ or be contrary to those expressed by other business areas or divisions of UBS as a result of using different assumptions and/or criteria. At any time, investment decisions (including whether to buy, sell or hold securities) made by UBS AG, its affiliates, subsidiaries and employees may differ from or be contrary to the opinions expressed in UBS research publications. Some investments may not be readily realizable since the market in the securities is illiquid and therefore valuing the investment and identifying the risk to which you are exposed may be difficult to quantify. UBS relies on information barriers to control the flow of information contained in one or more areas within UBS, into other areas, units, divisions or affiliates of UBS. Futures and options trading is considered risky. Past performance of an investment is no guarantee for its future performance. Some investments may be subject to sudden and large falls in value and on realization you may receive back less than you invested or may be required to pay more. Changes in FX rates may have an adverse effect on the price, value or income of an investment. This report is for distribution only under such circumstances as may be permitted by applicable law. Distributed to US persons by UBS Financial Services Inc. or UBS Securities LLC, subsidiaries of UBS AG. UBS Switzerland AG, UBS Deutschland AG, UBS Bank, S. A. , UBS Brasil Administradora de Valores Mobiliarios Ltda, UBS Asesores Mexico, S. A. de C. V. , UBS Securities Japan Co. , Ltd, UBS Wealth Management Israel Ltd and UBS Menkul Degerler AS are affiliates of UBS AG. UBS Financial Services Incorporated of Puerto Rico is a subsidiary of UBS Financial Services Inc. accepts responsibility for the content of a report prepared by a non-US affiliate when it distributes reports to US persons. All transactions by a US person in the securities mentioned in this report should be effected through a US-registered broker dealer affiliated with UBS, and not through a non-US affiliate. The contents of this report have not been and will not be approved by any securities or investment authority in the United States or elsewhere. UBS Financial Services Inc. is not acting as a municipal advisor to any municipal entity or obligated person within the meaning of Section 15 B of the Securities Exchange Act (the "Municipal Advisor Rule") and the opinions or views contained herein are not intended to be, and do not constitute, advice within the meaning of the Municipal Advisor Rule. UBS specifically prohibits the redistribution or reproduction of this material in whole or in part without the prior written permission of UBS and UBS accepts no liability whatsoever for the actions of third parties in this respect. Version as per September 2015. © UBS 2017. The key symbol and UBS are among the registered and unregistered trademarks of UBS. All rights reserved. 44

Appendix: Disclaimer UBS does not provide legal, tax or actuarial advice. You will be responsible for ensuring that your investment policy statement and other plan documents comply with ERISA, state or local laws, or other regulations or other requirements that apply to you. You should consult with your legal and tax advisors regarding those matters. Our services do not include a review of the performance or recommendations regarding whether a retirement plan should offer or continue to offer employer securities as an investment option under the plan. If our fees are based on the value of the assets in your plan, we will not include the value of the employer securities when we calculate our fees. Our investment searches will not include UBS affiliated/proprietary mutual or sub advised funds, unless requested by a nonretirement plan client. Inclusion of affiliated or proprietary mutual or sub advised funds in our investment searches raises a conflict of interest as purchasing those funds will result in increased compensation to UBS and/or a member of the UBS organization. While we can identify investment funds from an extensive list of options, our investment searches are limited to those which are offered by the Firm or for which the Firm has conducted a review. With regard to SMA Managers you select in the IC Program, we are not responsible for your choice of SMA Manager (in the non-discretionary IC Program), their day-to-day investment decisions, their performance, their compliance with applicable laws, rules or regulations and best execution obligations, their receipt of or compliance with your IPS, or any other matters within the SMA Manager’s control. Important Considerations of an Asset-Based Fee Option. You may pay more or less in a UBS Financial Services Inc. wrap-fee program than you might otherwise pay if you purchased the services separately. For example, depending on your asset allocation or strategy selection, you may find that the individual components of your strategy or allocation are available to you outside of the IC Program for more or less than you would pay in the IC Program. For important additional information, please see the UBS Financial Services' Disclosure Wrap Fee Brochure Form ADV for UBS-IC. Investment advisory services (including consulting and investment management) and brokerage/custody services are separate and distinct, differ in material ways and are governed by different laws and separate contracts. It is important that you carefully read the agreements and disclosures UBS provides to you about the products or services offered, including the Program. Products and services (including the Program) may not be available for residents in certain jurisdictions. This document does not constitute an offer to sell or a solicitation to offer to buy any security or product, and nothing in this document shall limit or restrict the particular terms of any specific offering or product. Offers will be made only to qualified investors by means of prospectus, offering memorandum or other document providing information as to the specifics of the offering or product. No offer of any security or product will be made in any jurisdiction in which the offer, solicitation or sale is not permitted or to any person to whom it is unlawful to make such offer, solicitation or sale. An investment adviser does not have to demonstrate or meet any minimum level of skill or training to register with the SEC. Wealth management services in the United States are provided by UBS Financial Services Inc. , a registered broker/dealer offering securities, trading, brokerage and related products and services. As a firm providing wealth management services to clients in the U. S. , we offer both investment advisory services and brokerage accounts. Advisory services and brokerage services are separate and distinct, differ in material ways and are governed by different laws and separate contracts. It is important that clients understand the ways in which we conduct business and that they carefully read the agreements and disclosures that we provide to them about the products or services we offer. For more information clients should speak with their Financial Advisor or visit our website at bs. com/workingwithus. u CIMA® is a registered certification mark of the Investment Management Consultants Association, Inc. in the United States of America and worldwide. Certified Financial Planner Board of Standards Inc. owns the certification marks CFP® and CERTIFIED FINANCIAL PLANNER™ in the U. S © UBS 2017. The key symbol and UBS are among the registered and unregistered trademarks of UBS. All rights reserved. UBS Financial Services Inc. is a subsidiary of UBS AG. Member FINRA/SIPC. 45

Contact Information Kristi Thelen, CFP® CIMA® Vice President – Wealth Management Institutional Consultant, UBS Institutional Consulting 404 -760 -3050 kristi. thelen@ubs. com J. Allen Wright, CIMA® Senior Wealth Strategy Associate Senior Institutional Consultant, UBS Institutional Consulting 404 -760 -3370 allen. wright@ubs. com The Peachtree Group UBS Financial Services Inc. 3455 Peachtree Rd NE Suite 1700 Atlanta, GA 30326 404 -760 -3000 http: //financialservices. ubs. com/team/peachtree/index. html 46

4678ce871dc3327cd56a785f83f6dd4b.ppt