BASIC ECONOMIC TERMINOLOGY-3.ppt

- Количество слайдов: 18

BASIC ECONOMIC TERMINOLOGY Money. Taxation.

Money is… § any object accepted as payment for goods and services and repayment of debts. § historically an market phenomena establishing a commodity money, but nearly all contemporary money systems are based on fiat money § The money supply of a country consists of currency (banknotes and coins) and bank money (the balance held in checking accounts and savings accounts).

Forms of money banknotes and coins

Main Functions § medium of exchange, § a unit of account, § a standard payment, § a store of value. § There have been many historical disputes regarding the combination of money's functions, some arguing that they need more separation and that a single unit is insufficient to deal with them all.

plus demand deposits (such")

Monetary aggregates § M 1 is currency (coins and bills) plus demand deposits (such as checking accounts); § M 2 is M 1 plus savings accounts and time deposits under $100, 000; § M 3 is M 2 plus larger time deposits and similar institutional accounts. § M 0 is base money, or the amount of money actually issued by the central bank of a country.

Types of money § Commodity money § Representative money § Fiat money § Currency

is to impose")

Tax § Tax To tax (from the Latin taxo; "I estimate") is to impose a financial charge or other levy upon a taxpayer (an individual or legal entity) by a state or the functional equivalent of a state such that failure to pay is punishable by law. Taxes are also imposed by many administrative divisions. Taxes consist of direct tax or indirect tax, and may be paid in money or as its labour equivalent (often but not always unpaid labour).

Tax rates § Taxes are most often levied as a percentage, called the tax rate. § An important distinction when talking about tax rates is to distinguish between the marginal rate and the effective (average) rate. § The effective rate is the total tax paid divided by the total amount the tax is paid on, while the marginal rate is the rate paid on the next dollar of income earned.

Tax systems § proportional, § progressive, § regressive, § lump-sum.

Kinds of taxes § § § Income tax Capital gains tax Corporate tax Property tax Inheritance tax Transfer tax Wealth tax Value added tax Sales tax Excise Tariff Other taxes

Tax haven § A tax haven is a state or a country or territory where certain taxes are levied at a low rate or not at all while offering due process, good governance, and a low corruption rate. § There are several definitions of tax havens. § The Economist has tentatively adopted the description by Geoffrey Colin Powell (former economic adviser to Jersey): "What. . . identifies an area as a tax haven is the existence of a composite tax structure established deliberately to take advantage of, and exploit, a worldwide demand for opportunities to engage in tax avoidance. " § According to other definitions, the central feature of a haven is that its laws and other measures can be used to evade or avoid the tax laws or regulations of other jurisdictions.

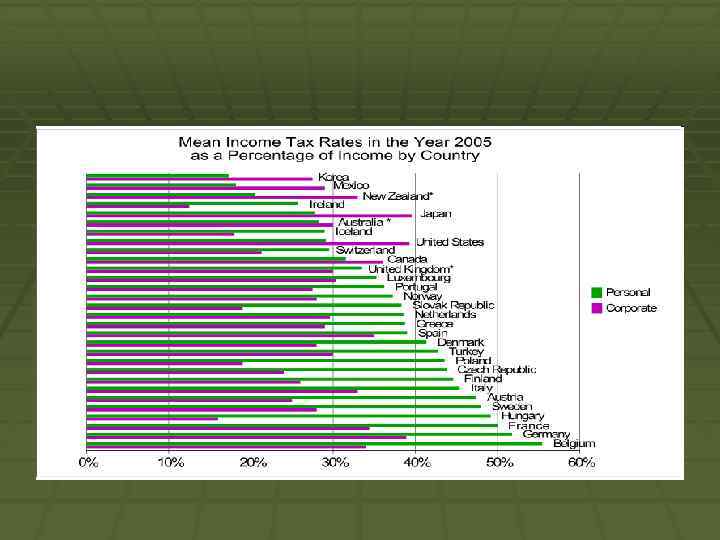

Tax rates of Europe Country Corporate tax Maximum Income tax rate Standard VAT rate Malta 35% 18% Belgium 33. 99% 50% 21% France 33. 33% 41% 19. 6% Italy 31. 4% 45% 21% Spain 30% 52% 21% Luxembourg 28. 59% 38. 95% 15% Greece 25% 45% 23% Belarus 24% 15% 20% Ukraine 23%, from 1. 01. 2012 - 21%, from 1. 01. 2013 - 17% 19%, from 1. 01. 2014 - 16% 20% Russia 20% 13% 18% (reduced rates 10% and 0%) Germany 15. 825 % (federal) plus 14. 35 % to 17. 5 % (local) 45% 19% Bosnia and Herzegovina 10% 5% 17% Albania 10% 20% Montenegro 9% 9% 17%

BASIC ECONOMIC TERMINOLOGY-3.ppt