4dba19e1b8f18323f6609fc87b56c44b.ppt

- Количество слайдов: 61

Associateships and Contracts

Associateships and Contracts

dentist(s) n n Proprietor, partner or corporate Non-owner (junior) dentist(s)") Associateship n Owner (senior) dentist(s) n n Proprietor, partner or corporate Non-owner (junior) dentist(s) n Employee or Independent Contractor

Associateship n Owner (senior) dentist(s) n n Proprietor, partner or corporate Non-owner (junior) dentist(s) n Employee or Independent Contractor

Why would a senior dr. want an associate? Economic reasons n Income generation n Utilization of capital base n Overhead reduction n Expanded hours of service n Excess patient load n Expanded dental services Non-Economic reasons • Buyer for practice • Reduce involvement in practice • Assist new grads • Trial period

Why would a senior dr. want an associate? Economic reasons n Income generation n Utilization of capital base n Overhead reduction n Expanded hours of service n Excess patient load n Expanded dental services Non-Economic reasons • Buyer for practice • Reduce involvement in practice • Assist new grads • Trial period

Why become an associate Economic reasons: n Income without risks n Increased clinical skills n Practice acquisitions n Financing not available Non-economic reasons n Transition time n Time to set goals n Evaluate location n Develop professional style n Gain business/manageme nt experience

Why become an associate Economic reasons: n Income without risks n Increased clinical skills n Practice acquisitions n Financing not available Non-economic reasons n Transition time n Time to set goals n Evaluate location n Develop professional style n Gain business/manageme nt experience

Advantages for associates to consider n n n n n Small or no capital outlay Opportunity to learn from experienced dentist Minimal organizational skill required No decision on staffing No decision on equipment No decision on office design Immediate patient pool Immediate income Time to adjust to practicing full-time Gain self-confidence

Advantages for associates to consider n n n n n Small or no capital outlay Opportunity to learn from experienced dentist Minimal organizational skill required No decision on staffing No decision on equipment No decision on office design Immediate patient pool Immediate income Time to adjust to practicing full-time Gain self-confidence

Disadvantages for associate to consider: n n n n Loss of autonomy Loss of self direction Junior partner-employee May not be allowed to contribute to office management May lose desire to contribute to office management Loss of time Risk of confrontation Must adust to facilities/equipment

Disadvantages for associate to consider: n n n n Loss of autonomy Loss of self direction Junior partner-employee May not be allowed to contribute to office management May lose desire to contribute to office management Loss of time Risk of confrontation Must adust to facilities/equipment

Potential for compromised principles n Must accept") Disadvantages for associate to consider (cont. ) Potential for compromised principles n Must accept fee schedules n Must accept staff n Postpones initial shock n Possible patient restrictions n Must obey other’s rules n Potential disappointments (amalgam line, etc. ) n

Disadvantages for associate to consider (cont. ) Potential for compromised principles n Must accept fee schedules n Must accept staff n Postpones initial shock n Possible patient restrictions n Must obey other’s rules n Potential disappointments (amalgam line, etc. ) n

Initial Considerations n n n Does the practice need an associate? - size of practice - number of new patients/month - is senior dentrist turning away patients that could be seen by an associate? Auxiliary personnel Facilities/equipment Senior man’s plans Patient load constraint

Initial Considerations n n n Does the practice need an associate? - size of practice - number of new patients/month - is senior dentrist turning away patients that could be seen by an associate? Auxiliary personnel Facilities/equipment Senior man’s plans Patient load constraint

Management considerations n Your ego n Personality n Has practice") Initial Considerations (cont. ) Management considerations n Your ego n Personality n Has practice been evaluated? n Gut reaction n

Initial Considerations (cont. ) Management considerations n Your ego n Personality n Has practice been evaluated? n Gut reaction n

Final Considerations n n n n n Your reasons for associateship Written letter of agreement Expense How patients allocated Employee vs. contractor Facility availability Staff Death/disability of either person Restrictive covenant

Final Considerations n n n n n Your reasons for associateship Written letter of agreement Expense How patients allocated Employee vs. contractor Facility availability Staff Death/disability of either person Restrictive covenant

Independent Contractor Indicators of Employee Status IRS 87 -41 n n n Personal delivery of service Continuing (ongoing) relationship Work on employer’s premises Use employer’s equipment / materials Owner controls employees n n n Hiring, Firing, Paying Worker cannot work in other location Worker cannot suffer a loss

Independent Contractor Indicators of Employee Status IRS 87 -41 n n n Personal delivery of service Continuing (ongoing) relationship Work on employer’s premises Use employer’s equipment / materials Owner controls employees n n n Hiring, Firing, Paying Worker cannot work in other location Worker cannot suffer a loss

Employer No Social Security / Medicare Tax (FICA) n") Independent Contractor Advantages to (Owner) Employer No Social Security / Medicare Tax (FICA) n No Unemployment Tax (FUTA / SUTA) n No Worker’s Compensation Insurance n No withholding income tax (Fed, State, Loc) n No retirement plan contribution n No benefits plan participation n

Independent Contractor Advantages to (Owner) Employer No Social Security / Medicare Tax (FICA) n No Unemployment Tax (FUTA / SUTA) n No Worker’s Compensation Insurance n No withholding income tax (Fed, State, Loc) n No retirement plan contribution n No benefits plan participation n

Employer n Restrictive Covenants less enforceable n n Virtually") Independent Contractor Disadvantages to (Owner) Employer n Restrictive Covenants less enforceable n n Virtually non-enforceable Can’t force employee compliance

Independent Contractor Disadvantages to (Owner) Employer n Restrictive Covenants less enforceable n n Virtually non-enforceable Can’t force employee compliance

New Practitioner Partnerships n Advantages Save expenses n Joint purchases n Psychological support n n Disadvantages Sufficiency of patient base n Mutual inhibition of growth n Group conflict n Long term commitment to group practice n

New Practitioner Partnerships n Advantages Save expenses n Joint purchases n Psychological support n n Disadvantages Sufficiency of patient base n Mutual inhibition of growth n Group conflict n Long term commitment to group practice n

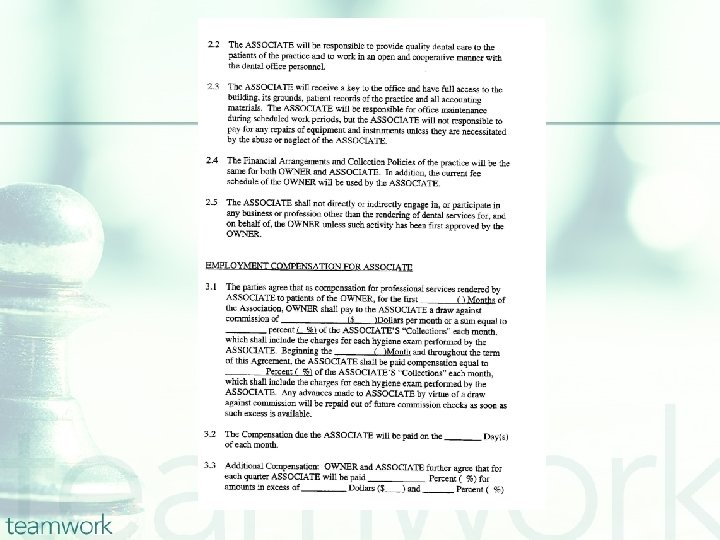

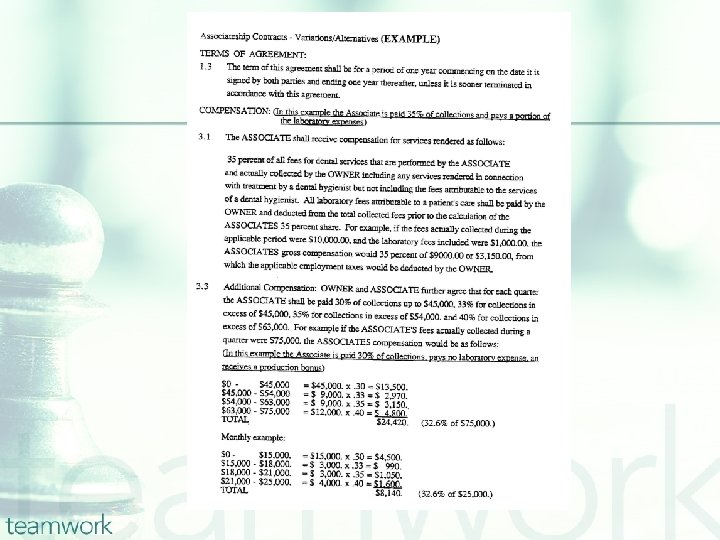

Financial Structure of Associateships n Compensation Mechanism Should … Allow a profit for the owner n Allow a profit for the associate n Provide incentive for the associate to produce n Provide incentives for the associate to collect n Provide incentives for both to be efficient n Be fair to both n

Financial Structure of Associateships n Compensation Mechanism Should … Allow a profit for the owner n Allow a profit for the associate n Provide incentive for the associate to produce n Provide incentives for the associate to collect n Provide incentives for both to be efficient n Be fair to both n

Office Expenses by Category Expenses as a % of Collections Occupancy 8. 8% Clerical Wages 9. 6% Non-Operating Supplies and Expenses 11. 9% Chairside Wages 18. 4% Professional Supplies and Expenses 15. 5% Total Costs 62. 4% Total Profit 35. 8% Blair / Mc. Gill Advisory

Office Expenses by Category Expenses as a % of Collections Occupancy 8. 8% Clerical Wages 9. 6% Non-Operating Supplies and Expenses 11. 9% Chairside Wages 18. 4% Professional Supplies and Expenses 15. 5% Total Costs 62. 4% Total Profit 35. 8% Blair / Mc. Gill Advisory

") Financial Structure of Associateships Advantages Disadvantages Fixed Salary Easy bookkeeping No incentive (assoc. ) Easy budgeting Security for assoc. Owner can lose No A/R if break-up Time Sharing High independence No patients for assoc. Lower OH if offset hours Working undesirable hours Duplication of services Competition for patients

Financial Structure of Associateships Advantages Disadvantages Fixed Salary Easy bookkeeping No incentive (assoc. ) Easy budgeting Security for assoc. Owner can lose No A/R if break-up Time Sharing High independence No patients for assoc. Lower OH if offset hours Working undesirable hours Duplication of services Competition for patients

Financial Structure of Associateships Advantages Disadvantages % Gross Production Easy bookkeeping No incentive (assoc. ) to collect Some security for assoc. Owner must collect Incentive for assoc. to produce No A/R if break-up (Owner controls policies / procedures) % Collections Incentive for assoc. to produce Delayed compensation for assoc. Incentive for assoc. to collect Assoc. does not control collections Complex bookkeeping A/R Disposition if break up

Financial Structure of Associateships Advantages Disadvantages % Gross Production Easy bookkeeping No incentive (assoc. ) to collect Some security for assoc. Owner must collect Incentive for assoc. to produce No A/R if break-up (Owner controls policies / procedures) % Collections Incentive for assoc. to produce Delayed compensation for assoc. Incentive for assoc. to collect Assoc. does not control collections Complex bookkeeping A/R Disposition if break up

Financial Structure of Associateships n Hybrid Methods Salary with a bonus for production n Variable commission n Collections net lab expenses n Commission with a floor n Shared fixed expenses, allocated variable expenses n

Financial Structure of Associateships n Hybrid Methods Salary with a bonus for production n Variable commission n Collections net lab expenses n Commission with a floor n Shared fixed expenses, allocated variable expenses n

How are associates paid? Usually % n Based on overhead n Usually 25 -40% n Lab split? n Senior pays all other expenses n Senior provides staff/materials n Paid on collection/production n

How are associates paid? Usually % n Based on overhead n Usually 25 -40% n Lab split? n Senior pays all other expenses n Senior provides staff/materials n Paid on collection/production n

Variable Commission Example Collections Percentage Applied 0 – 10, 000 25% 10, 001 – 12, 000 27% 12, 001 – 15, 000 30% 15, 001 – 18, 000 32% 18, 001 – 21, 000 34% 21, 001 – 25, 000 36% 25, 001 – 30, 000 38% 30, 001 + 40%

Variable Commission Example Collections Percentage Applied 0 – 10, 000 25% 10, 001 – 12, 000 27% 12, 001 – 15, 000 30% 15, 001 – 18, 000 32% 18, 001 – 21, 000 34% 21, 001 – 25, 000 36% 25, 001 – 30, 000 38% 30, 001 + 40%

Gross Production Adjustments - Uncollectibles (Charge Back) Collections -") General Compensation Formula (Production Based) Gross Production Adjustments - Uncollectibles (Charge Back) Collections - Lab Charges ((Professional expenses)) Income Produced Apply percentage (30% – 35%) ((Professional expenses)) Taxes Net (Spendable) Income This makes this basically a Collections Based

General Compensation Formula (Production Based) Gross Production Adjustments - Uncollectibles (Charge Back) Collections - Lab Charges ((Professional expenses)) Income Produced Apply percentage (30% – 35%) ((Professional expenses)) Taxes Net (Spendable) Income This makes this basically a Collections Based

Gross Collections - Lab Charges ((Professional expenses )) Income") General Compensation Formula (Collection Based) Gross Collections - Lab Charges ((Professional expenses )) Income Produced Apply percentage (30% – 35%) ((Professional expenses)) Taxes Net (Spendable) Income

General Compensation Formula (Collection Based) Gross Collections - Lab Charges ((Professional expenses )) Income Produced Apply percentage (30% – 35%) ((Professional expenses)) Taxes Net (Spendable) Income

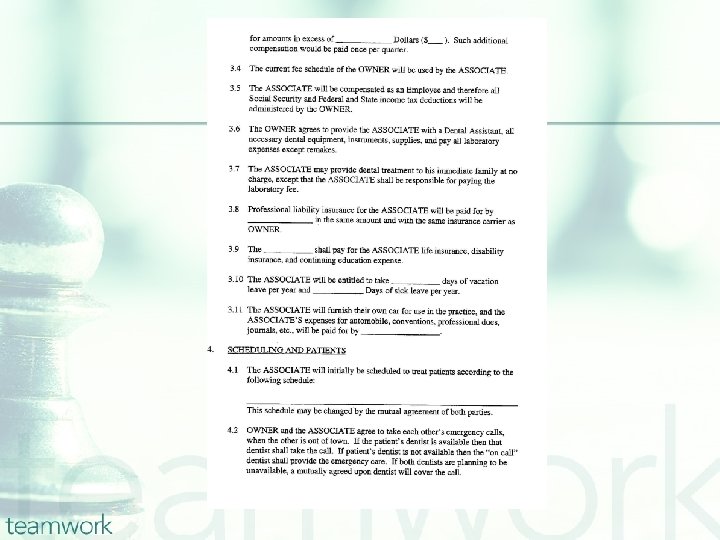

Lab Fees n Some Contracts Deduct Lab Fees n n Deduct Full Lab Fee vs. Partial Lab Fee How are Fees Deducted I am not a fan of Lab Fee Deduction However, consideration should be given to remakes.

Lab Fees n Some Contracts Deduct Lab Fees n n Deduct Full Lab Fee vs. Partial Lab Fee How are Fees Deducted I am not a fan of Lab Fee Deduction However, consideration should be given to remakes.

Show me the Math!

Show me the Math!

More Math! Class II Restoration Class II $200 less 60% OH $120 Profit $ 80 Procedure Time – 30 min Hourly profit - $160 Crown $1000 less Lab fee $ 200 Total $ 800 less 60% OH $ 480 Profit $ 320 Procedure Time – 1. 5 hrs Hourly profit - $213. 33

More Math! Class II Restoration Class II $200 less 60% OH $120 Profit $ 80 Procedure Time – 30 min Hourly profit - $160 Crown $1000 less Lab fee $ 200 Total $ 800 less 60% OH $ 480 Profit $ 320 Procedure Time – 1. 5 hrs Hourly profit - $213. 33

What about the PPO office? Class II Restoration Class II $100 less 70% OH $ 70 Profit $ 30 Procedure Time – 30 min Hourly profit - $60 Crown $ 600 less Lab fee $ 120 Total $ 480 less 70% OH $ 336 Profit $ 144 Procedure Time – 1. 5 hrs Hourly profit - $96

What about the PPO office? Class II Restoration Class II $100 less 70% OH $ 70 Profit $ 30 Procedure Time – 30 min Hourly profit - $60 Crown $ 600 less Lab fee $ 120 Total $ 480 less 70% OH $ 336 Profit $ 144 Procedure Time – 1. 5 hrs Hourly profit - $96

Hourly (assume 30 min) $200") Associate with Lab Deducted Class II Associate pay (35%) Hourly (assume 30 min) $200 $ 70 $140 Crown Associate pay (35%) less Lab Fee Associate Net Hourly (assume 1. 5 hrs) $1000 $ 350 $ 200 $ 150 $ 100 Remember the office profit was $160, so practice still had $20 profit per hour Office profit was again $213, so practice had $113 profit per hour

Associate with Lab Deducted Class II Associate pay (35%) Hourly (assume 30 min) $200 $ 70 $140 Crown Associate pay (35%) less Lab Fee Associate Net Hourly (assume 1. 5 hrs) $1000 $ 350 $ 200 $ 150 $ 100 Remember the office profit was $160, so practice still had $20 profit per hour Office profit was again $213, so practice had $113 profit per hour

$ 350 Hourly (assume 1.") Associate with Lab Deducted Crown $1000 Associate pay (35%) $ 350 Hourly (assume 1. 5 hrs) $ $233. 33 Office less lab fee True office production less 60% OH less associate’s pay Net Office Profit Hourly Profit $1000 $ 200 $ 800 $ 480 $ 350 $ 250 $ 125

Associate with Lab Deducted Crown $1000 Associate pay (35%) $ 350 Hourly (assume 1. 5 hrs) $ $233. 33 Office less lab fee True office production less 60% OH less associate’s pay Net Office Profit Hourly Profit $1000 $ 200 $ 800 $ 480 $ 350 $ 250 $ 125

Lab Cases – Who Pays? Who Cares? Assume: $600 Procedure, $150 Lab, OH=$250, Split=33%/66% Assoc. Pays Assoc Owner Pays Assoc. Owner Fee 600 Split (a) 200 400 200 150 0 0 150 Assoc. Owner 400 Lab Cost Split 600 150 450 OH 250 Split(b) Net 250 150 200 0 300 150 50

Lab Cases – Who Pays? Who Cares? Assume: $600 Procedure, $150 Lab, OH=$250, Split=33%/66% Assoc. Pays Assoc Owner Pays Assoc. Owner Fee 600 Split (a) 200 400 200 150 0 0 150 Assoc. Owner 400 Lab Cost Split 600 150 450 OH 250 Split(b) Net 250 150 200 0 300 150 50

Bottom Line n 1 st year expect $70, 000 -100, 000 n n 2 nd year expect $90, 000 -120, 000 n n Initially averaging slightly less Some do better, some do worse Owner’s make more n However, have a lot of initial debt

Bottom Line n 1 st year expect $70, 000 -100, 000 n n 2 nd year expect $90, 000 -120, 000 n n Initially averaging slightly less Some do better, some do worse Owner’s make more n However, have a lot of initial debt

Do the Calculations n Look at an average patient schedule n Determine if you think your schedule will be the same n n Remember you will be slower initially Determine daily production base on Office Fees Calculate your compensation based on your contract Under Estimate n No Shows, Holidays, Continuing Ed, Vacation

Do the Calculations n Look at an average patient schedule n Determine if you think your schedule will be the same n n Remember you will be slower initially Determine daily production base on Office Fees Calculate your compensation based on your contract Under Estimate n No Shows, Holidays, Continuing Ed, Vacation

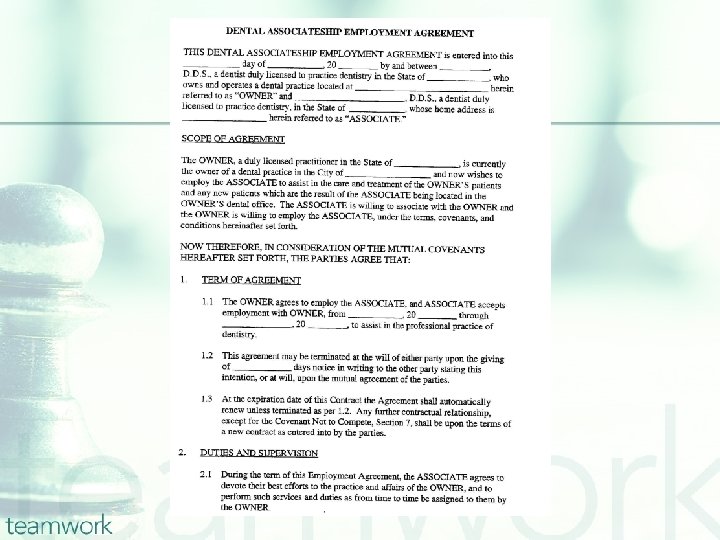

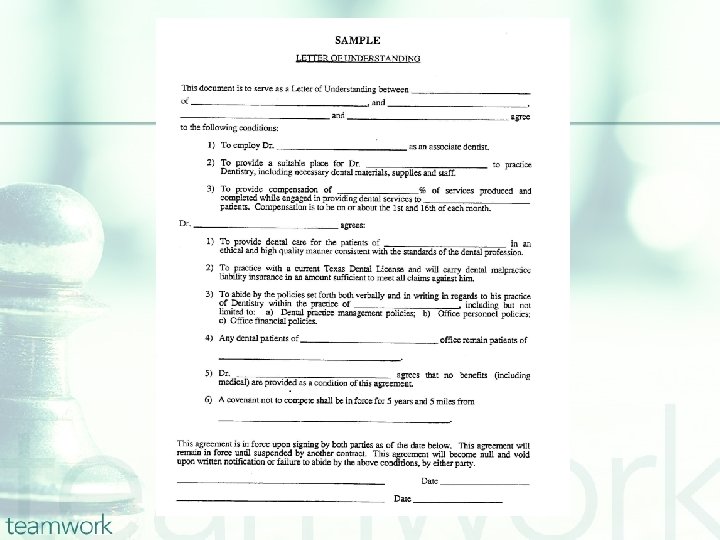

n n n Should be written Consult Attorney Duration of contract") Associateship Contracts (1) n n n Should be written Consult Attorney Duration of contract Employee vs Independent Contractor Compensation Management Responsibilities Patient Allocation Office Coverage (Call Schedule) Patient Records (ownership) Nature of Work Employee Benefits (if any) Time off (paid / unpaid)

Associateship Contracts (1) n n n Should be written Consult Attorney Duration of contract Employee vs Independent Contractor Compensation Management Responsibilities Patient Allocation Office Coverage (Call Schedule) Patient Records (ownership) Nature of Work Employee Benefits (if any) Time off (paid / unpaid)

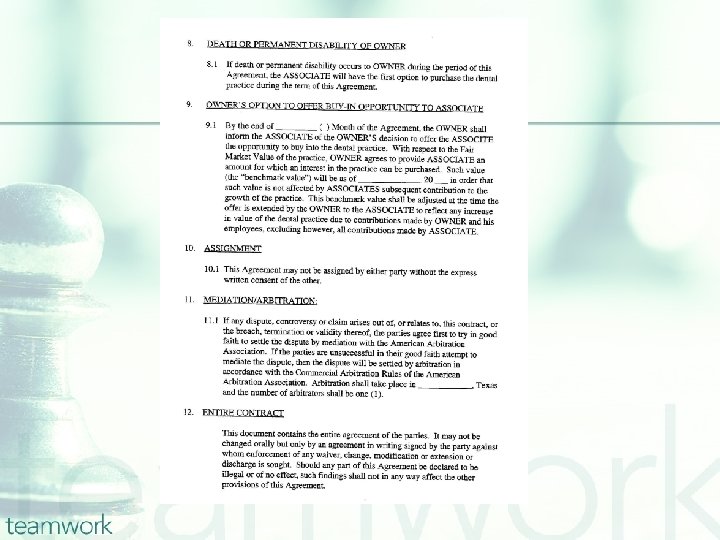

Death / Disability of either party n Dissolution n Valid reasons") Associateship Contracts (2) Death / Disability of either party n Dissolution n Valid reasons n Patients n Restrictive covenant n Accounts receivable n Staff n Modification of contract n Renewal n

Associateship Contracts (2) Death / Disability of either party n Dissolution n Valid reasons n Patients n Restrictive covenant n Accounts receivable n Staff n Modification of contract n Renewal n

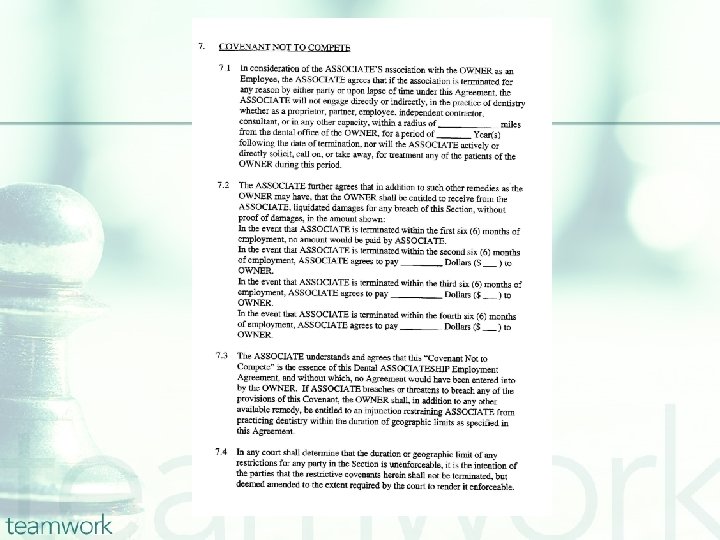

n Buy – Sell Provisions Right of first refusal n Mandatory") Associateship Contracts (3) n Buy – Sell Provisions Right of first refusal n Mandatory purchase n Partnership offer n Price determination n n Restrictive Covenant Associate leaves n Associate buys n

Associateship Contracts (3) n Buy – Sell Provisions Right of first refusal n Mandatory purchase n Partnership offer n Price determination n n Restrictive Covenant Associate leaves n Associate buys n

Problem Associateships Associateship that lasts more than 2 years before buy-in n Owner needs income (production) n Associate does all the managed care n Associate does all the “Phase 1” n Associate is assigned to a satellite office n

Problem Associateships Associateship that lasts more than 2 years before buy-in n Owner needs income (production) n Associate does all the managed care n Associate does all the “Phase 1” n Associate is assigned to a satellite office n

Associateship must be beneficial to both parties. If either party dissatisfied, then relationship will fail.

Associateship must be beneficial to both parties. If either party dissatisfied, then relationship will fail.

Lack of written associateship agreement n Negative production impact") Common Reasons Associateships Fail (1) Lack of written associateship agreement n Negative production impact on owner n Associate’s unrealistic income expectations n Incompatible philosophies of practice n Inability of the practice to support an additional full time dentist n Associate’s unwillingness to adapt to practice policies and procedures n

Common Reasons Associateships Fail (1) Lack of written associateship agreement n Negative production impact on owner n Associate’s unrealistic income expectations n Incompatible philosophies of practice n Inability of the practice to support an additional full time dentist n Associate’s unwillingness to adapt to practice policies and procedures n

n Host sets compensation too high Profitability n Income") Common Reasons Associateships Fail (2) n Host sets compensation too high Profitability n Income decrease during buy-in n General lack of patients n Internal referral of specialty work n Inability to see the difference for being paid to do dentistry and ownership n Spouse problems (usually associate’s) n

Common Reasons Associateships Fail (2) n Host sets compensation too high Profitability n Income decrease during buy-in n General lack of patients n Internal referral of specialty work n Inability to see the difference for being paid to do dentistry and ownership n Spouse problems (usually associate’s) n

n n n n Associate’s unwillingness to devote sufficient") Common Reasons Associateships Fail (3) n n n n Associate’s unwillingness to devote sufficient effort to building the practice Associate’s unwillingness to take owner’s advise because he thinks he knows more than the “outdated” owner Associate’s unrealistic income expectations Owner’s unwillingness to assign patients fairly to associate Owner’s unwillingness to spend sufficient time with the associate Owner’s unwillingness to relinquish any control to associate Owner’s unwillingness to sell all or a portion of the practice to associate Owner’s unwillingness to listen to ideas put forth by the associate

Common Reasons Associateships Fail (3) n n n n Associate’s unwillingness to devote sufficient effort to building the practice Associate’s unwillingness to take owner’s advise because he thinks he knows more than the “outdated” owner Associate’s unrealistic income expectations Owner’s unwillingness to assign patients fairly to associate Owner’s unwillingness to spend sufficient time with the associate Owner’s unwillingness to relinquish any control to associate Owner’s unwillingness to sell all or a portion of the practice to associate Owner’s unwillingness to listen to ideas put forth by the associate

Out Clause n Allows either party to terminate contract n Specific Time Period n Usually n n 1 to 6 month 1 month to short n Not enough time to finish treatment started n Not enough time to find a new job 6 months to long n A long time to live in a bad situation n Suggest 2 to 3 month (60 to 90 day)

Out Clause n Allows either party to terminate contract n Specific Time Period n Usually n n 1 to 6 month 1 month to short n Not enough time to finish treatment started n Not enough time to find a new job 6 months to long n A long time to live in a bad situation n Suggest 2 to 3 month (60 to 90 day)

Competition Agreement n Distance from practice 2 miles in a large metropolitan area n 10 -15 miles in suburban area n 20+ miles in a rural area (especially if next dentist is more that 100 miles away) n n Time Period n Usually 1 to 2 years from the time the contract is terminated

Competition Agreement n Distance from practice 2 miles in a large metropolitan area n 10 -15 miles in suburban area n 20+ miles in a rural area (especially if next dentist is more that 100 miles away) n n Time Period n Usually 1 to 2 years from the time the contract is terminated

Competition Agreement n Generally not easily enforceable n Independent Contractor n Minimal n Consideration n Legal n enforceability fees to fight – Win or Lose Some contracts define a damages/losses in dollar terms n Increased enforceability

Competition Agreement n Generally not easily enforceable n Independent Contractor n Minimal n Consideration n Legal n enforceability fees to fight – Win or Lose Some contracts define a damages/losses in dollar terms n Increased enforceability

Competition Agreement n Working for a clinic/practice with more than one locations n The covenant should only state a distance from the primary (or single) office you work in (even if you work at other locations)

Competition Agreement n Working for a clinic/practice with more than one locations n The covenant should only state a distance from the primary (or single) office you work in (even if you work at other locations)

Goal Setting n Locating n Interviewing n Negotiating n") Locating Associateships (How) Goal Setting n Locating n Interviewing n Negotiating n

Locating Associateships (How) Goal Setting n Locating n Interviewing n Negotiating n

Dental Society meetings n AGD website n Family, Friends, Mentors n") Locating Associateships (Where) Dental Society meetings n AGD website n Family, Friends, Mentors n Extramural rotations n Placement Programs n Dental Suppliers n

Locating Associateships (Where) Dental Society meetings n AGD website n Family, Friends, Mentors n Extramural rotations n Placement Programs n Dental Suppliers n

How might a senior dentist locate an associate? n n n n n Individual contacts Dental School placement services National and State dental organizations Practice consultants/brokers Dental Supply Companies Ads in dental publications Colleagues/alumni Advanced Education programs Dental School faculty

How might a senior dentist locate an associate? n n n n n Individual contacts Dental School placement services National and State dental organizations Practice consultants/brokers Dental Supply Companies Ads in dental publications Colleagues/alumni Advanced Education programs Dental School faculty

Locating associateship opportunities n n n n n Start early (up to one year in advance) Dental School placement service State society placement service Dental Supply companies Dentists in your area of choice Classified ads in dental publications Consultants/Brokers Bulletin boards Visit dental meetings

Locating associateship opportunities n n n n n Start early (up to one year in advance) Dental School placement service State society placement service Dental Supply companies Dentists in your area of choice Classified ads in dental publications Consultants/Brokers Bulletin boards Visit dental meetings

Locating Opportunities: n n Dental School Placement Service State society placement service Local dental society newsletter Supply Reps n n n State society journals Practice consultants Lab Techs Word of Mouth Networking Direct Mailings

Locating Opportunities: n n Dental School Placement Service State society placement service Local dental society newsletter Supply Reps n n n State society journals Practice consultants Lab Techs Word of Mouth Networking Direct Mailings

Have Attorney Review Contract After you have worked out all the other issues, you need to have someone review your contract for legal content. n You will not be able to determine all the Legal-eze n n Example: n Disputes will be managed in a Court of Nebraska n Disputes will be managed in a Court in Nebraska

Have Attorney Review Contract After you have worked out all the other issues, you need to have someone review your contract for legal content. n You will not be able to determine all the Legal-eze n n Example: n Disputes will be managed in a Court of Nebraska n Disputes will be managed in a Court in Nebraska

The trouble with the rat race is that even if you win, you’re still a rat. LILY TOMLIN

The trouble with the rat race is that even if you win, you’re still a rat. LILY TOMLIN

Questions?

Questions?