42b3b1c6e490f5dbeb5b1b3beba134dd.ppt

- Количество слайдов: 25

Apartment Recommendations Update Housing and Planning Scrutiny sub group 12 th November 2008

Recommendation 1 • That planning officers monitor the number of applications received for apartments in comparison to houses within the city

Ø Total dwellings with planning permission 2006 -08: Dwellings with planning permission 2006 -2008 by House Type Date Total Houses Apartments 31/03/2006 11, 242 1, 716 9, 526 15. 3% 84. 7% 31/03/2007 16, 953 1, 956 14, 997 11. 5% 88. 5% 31/03/2008 17, 250 2, 087 15, 163 12. 1% 87. 9% Ø Dwellings with planning permission at 31 st March 08 (by type and area): Location Total Dwellings Houses (%) Apartments Central Salford 15, 213 9% 91% Salford West 2, 037 37% 63% TOTAL 17, 250 12. 1% 87. 9% Ø Comparison to other Greater Manchester districts

:")

Ø Total dwelling completions 2001 -08 (by type):

: Location Central Salford West TOTAL Total")

Dwellings completed 2007 -08 (by type and area): Location Central Salford West TOTAL Total Dwellings Houses (%) Apartments 2, 136 22% 78% 630 33% 67% 2, 766 24. 26% 75. 74%

Recommendations 2 and 7 • As the research undertaken points to the apartment market being both transient and investor led. That planning officers continue to monitor this sector of the market especially in relation to long term planning for the city and sustainable neighbourhoods. • Members recommend that vacancy rates are monitored in future by developments as well as by ward by planning officers. This will ensure that specific developments or pockets of the city do not become susceptible to high vacancy rates.

Transient and investor led market Ø Short term lets, Buy-to-leave, Buy-to-let • Solution to affordability? • Investor purchasing of older property Ø Lack of accurate quantitative analysis; anecdotal evidence – Housing Moves Study Ø Marketing suite surveys being undertaken; – Saltra – 80% PR; 20% OO – Spectrum, Blackfriars Road – 50% PR; 50% OO – Developments with housing are less influenced by private rented sector; Agecroft; Oaklands Road.

2002 -03 Vacancy rate 2003 -04")

Vacancy Rates Period Scheme completed (apartment schemes only) 2002 -03 Vacancy rate 2003 -04 2004 -05 2005 -06 2006 -07 8. 40% 13. 70% 21. 30% 17. 30% 40. 80% ØInformation from council tax records – caution with data ØVacancy rates generally decline the longer a scheme has been complete ØLarge schemes completed in: • 2003 -2004: vacancy rates of between 7. 7% (City Point 2) and 21. 1% (The Bridge) • 2006 -2007: vacancy rates between 25. 5% (Dock 5) and 46. 7% (Fusion) ØFurther research needed to assess why vacancy rates can differ so much by scheme

Turnover Rates Ø Suspect significant difference between turnover rate in apartments and houses Ø Further research needed Policy Context: Ø No current planning policy on vacancy / investor sales • Development Partnerships offer some control Ø Core Strategy Issues and Options • Submission of sales strategy • Conditions to prevent short lets to reduce turnover

Recommendation 3 • Planning officers are requesting that a certain amount of 3 bed apartments are included in developments. However those developers attending the meeting felt that these were proving difficult to sell. Therefore members recommend that further dialogue takes place with planning officers and developers to look further into this issue.

Ø Housing Planning Guidance – seek to achieve significant proportion of 3 bedroom apartments • In practice aim for 10% - why? • Aim is to secure not just 3 bed penthouses • “Success” - 44 x 3 bed apartments completed 2007 -08; 578 with planning permission Ø Contrary evidence to merits of 3 bed apartments • DJ Housing Position Statement – 3 bed apartments are “not the answer” (well designed unique products are though) • Dandara - 3 bed apartments will go to investors who will use them for serviced apartments • LPC looking at 3 bed duplex over duplex apartments • Developers are providing the units - no Appeals Ø Core Strategy Issues and Options • Deliver a broad mix of sizes, including 3 beds – out for consultation

Recommendation 4 • That planning officers continue dialogue with Estate Agents and developers as they are able to give an insight as to what is happening within the housing market.

Ø Housing Position Statement • One to One consultation meetings • Nikal Developments, Countryside Properties, LPC Living, Dandara, Urban Splash, Peel Holdings. • Stakeholder Workshops • Stakeholder Questionnaire Ø Ongoing discussions with developers over potential amendments to schemes in light of the “credit-crunch” Ø Estate Agents questionnaire • Poor response; last questionnaire sent in January 2008 • New method of engaging with estate agents to be developed

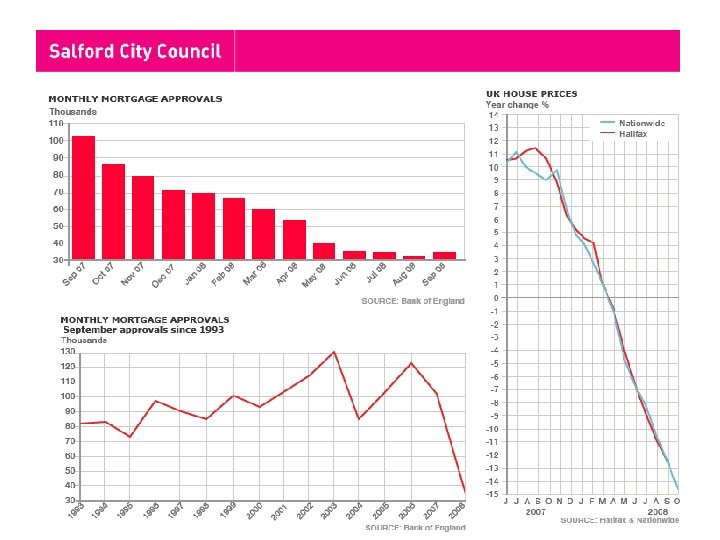

: • House prices dropped")

Ø General trends from national and local media (UK figures): • House prices dropped 14. 6% in the last year • 1. 2 m households expected to be in negative equity within 2 years • Amount of time from the time of going on the market to going under offer rose (from 7. 4 weeks in October last year to 11. 9 weeks now) • Number of property sales fallen by 53% in last year • Number of repossessions in the second quarter of 2008 up 71% compared with a year earlier. • 0. 16% (1, 800 dwellings) repossessed in first half of 2008 • 18% dip in buy to let mortgages in first half of 2008

Salford specific market conditions Ø “HMR Dashboard” • • • House prices continuing to fall Number of sales has dropped dramatically Void properties are increasing Slight increase in the number of auctions – success rate falling Proportion of repossessed properties has increased Ø Partial review of development activity underway Ø Some schemes will not happen in the short term – BS Construction (Greengate), ASK (Greengate and Clippers Quay) Vermont (Foundry Wharf), Chapel Wharf (Dandara)

Recommendation 5 • That further work is undertaken by planning officers to monitor existing policies and amend where necessary to ensure that the mature suburbs are not suffering a detrimental change due to the introduction of high density apartments within the area.

Policy Context Ø Existing policies • UDP Policy H 1 – “balanced mix of dwellings” • Housing Planning Guidance (Policies HOU 1 and HOU 2) Ø Core Strategy Issues and Options • 80 -90% “family orientated dwellings” in Salford West, Broughton Park / Higher Broughton, Claremont and northern part of Weaste and Seedley. • 50 -70% in rest of Central Salford excluding Regional Centre • 10 -20% of dwellings in the regional centre, district centres and local centres • Redevelopment of existing dwellings (options 2 & 4)

Recommendation 6 • That information is provided to members to show where high density dwelling is introduced, especially in the suburban areas that consideration has been given to the increase in traffic, and the impact on local services including draining, flooding and highways as a result of the new developments and that monitoring and appropriate measures are taking place by planning officers.

Ø The Impact of new developments in terms of drainage, flooding and highways is assessed as part of any planning application Ø Building for Life • • Character Roads, parking and pedestrianisation Design and construction Environment and community Ø Particular schemes for investigation?

Recommendation 8 • It is important that the landlord accreditation scheme is promoted and implemented throughout the city, especially due to the increase in the numbers of private rented accommodation and new landlords within Salford. Housing and planning officers to report back to members when required.

Landlord accreditation Ø Does not replace legal obligations Ø Market support have been promoting the service • • • Area based meetings in Langworthy in Broughton Property Investors show Salford University event Resident meetings Landlord Forums Ø Incentives for joining the scheme Ø Progress and targets

Landlord Licensing Ø Compulsory for HMOs Ø Selective licensing of other private dwellings • Parts of Seedley and Langworthy are covered • Broughton and Kersal / Charlestown • Should only be used in priority areas • Failure to apply for a licence Ø Benefits of licensing • Working closely with all parties

Recommendation 9 • That planning officers provide information to members in relation to the PFI areas and future programmes, as to how these are programmed into the strategies and accounted for in planning terms in relation to the number of new homes within the city.

Ø Regeneration Areas • PFI • New Deal for Communities • Development Partnerships § Ordsall – LPC § Miller Homes and Inspired Development § The Higher Broughton Partnership Ø Core Strategy Issues and Options • Identifies areas of major change • Number of new homes in different areas reflects regeneration proposals • Growth point is factored in

42b3b1c6e490f5dbeb5b1b3beba134dd.ppt