ba6ec2a092a454ec7aee837c58af3f25.ppt

- Количество слайдов: 28

~ An Insider’s Perspective On Marketing Insurance and Trusts to Charity ~ Henry T. Rubin, JD Executive Director, Major and Planned Gifts Albert Einstein College of Medicine 212 917 710 -2098 hrubin@yu. edu

~ An Insider’s Perspective On Marketing Insurance and Trusts to Charity ~ Henry T. Rubin, JD Executive Director, Major and Planned Gifts Albert Einstein College of Medicine 212 917 710 -2098 hrubin@yu. edu

What 3 Things Do Charities Really Want? Operating Income: steady, sustainable sources of annual revenue Endowments: to replace lost donor annual revenue for perpetuity

What 3 Things Do Charities Really Want? Operating Income: steady, sustainable sources of annual revenue Endowments: to replace lost donor annual revenue for perpetuity

What Do Major Donors Want Most? • To make an “Impact” Gift • To be Seen as Leaders • To Reduce Taxes • To Help Family • To Establish Legacy …. . the Common Denominator? ? Quid pro quo Psychological, social, emotional, esteem and control

What Do Major Donors Want Most? • To make an “Impact” Gift • To be Seen as Leaders • To Reduce Taxes • To Help Family • To Establish Legacy …. . the Common Denominator? ? Quid pro quo Psychological, social, emotional, esteem and control

~ Tips to sell to charity ~ • Sell cash, not deferred goods. • Make sure your deferred gift will be additive with cash. • Don’t go through the advancement office or even the President’s office. • Go through a major board member – and get him to lead the board by example! • Pay to play to gain credibility • Join a committee • Return part of the premium • Don’t get too sophisticated so no one understands you • Make certain to your advancement officer and donor that your vehicle will not cannibalize the donor’s annual gift.

~ Tips to sell to charity ~ • Sell cash, not deferred goods. • Make sure your deferred gift will be additive with cash. • Don’t go through the advancement office or even the President’s office. • Go through a major board member – and get him to lead the board by example! • Pay to play to gain credibility • Join a committee • Return part of the premium • Don’t get too sophisticated so no one understands you • Make certain to your advancement officer and donor that your vehicle will not cannibalize the donor’s annual gift.

Why Insurance is “Such as Awful Charitable Gift” and other Myths • “It will cannibalize the donor’s annual gift”. • “We need current cash”. • “We’ll have to wait 20 years for the money”. • “The Board hates it”. • “We just don’t do it. ”

Why Insurance is “Such as Awful Charitable Gift” and other Myths • “It will cannibalize the donor’s annual gift”. • “We need current cash”. • “We’ll have to wait 20 years for the money”. • “The Board hates it”. • “We just don’t do it. ”

Destroy the Myths! Show trusts, insurance and annuities provide cash to charities

Destroy the Myths! Show trusts, insurance and annuities provide cash to charities

Donor Opportunities Problems Not For Profit Answers Bequests Charity does not have present use of any cash ACCELERATE BEQUESTS: turn bequest into cash and insurance. Donor gets tax deduction and legacy for less. Perpetual Annual Gift Donor can make VIRTUAL ENDOWMENT modest annual gifts, “endow” with revocable but cannot afford deferred gift; insurance, endowment annuity, bequest, etc. Roth Conversions Great idea, but donor must pay significant up front taxes Cash Gift to charity provides perfect deduction to “absorb” the tax incurred by Roth conversion. Gift Annuity or charitable remainder trust Charity has to wait until end of beneficiary’s life before it receives cash. Apply a portion of annual increased cash to donor for annual cash gifts to charity – and to buy insurance to provide fund to support annual gift forever.

Donor Opportunities Problems Not For Profit Answers Bequests Charity does not have present use of any cash ACCELERATE BEQUESTS: turn bequest into cash and insurance. Donor gets tax deduction and legacy for less. Perpetual Annual Gift Donor can make VIRTUAL ENDOWMENT modest annual gifts, “endow” with revocable but cannot afford deferred gift; insurance, endowment annuity, bequest, etc. Roth Conversions Great idea, but donor must pay significant up front taxes Cash Gift to charity provides perfect deduction to “absorb” the tax incurred by Roth conversion. Gift Annuity or charitable remainder trust Charity has to wait until end of beneficiary’s life before it receives cash. Apply a portion of annual increased cash to donor for annual cash gifts to charity – and to buy insurance to provide fund to support annual gift forever.

The Charitable Lead Trust: Apply Historically Low Interest Rates to Dramatically Reduce Estate Tax! Estate Tax Saved: Assumptions: $10, 000 Lead Annuity Trust 21 Years, 3% annually to charity 2 % Federal 7520 Rate as of February 2015

The Charitable Lead Trust: Apply Historically Low Interest Rates to Dramatically Reduce Estate Tax! Estate Tax Saved: Assumptions: $10, 000 Lead Annuity Trust 21 Years, 3% annually to charity 2 % Federal 7520 Rate as of February 2015

The Charitable Remainder Trust KEEP SELL CRT E ASSETS$100, 000 EVE$100, 000 RAG L -0 - 20, 000 AVE BEEN -0 ULD H THAT WO APITAL $100, 000 $80, 000 D C $100, 000 TO BUIL TAXED FAMILY R YOUR FO 7% 0 Annual 5% Annual up to 80% ins; Income Annual n capital ga ge o 23% levera Income on pensions) $70, 000 (Up to leverage $40, 000 Estate tax (Double Tax) Income Tax Deduction: $400, 000 Avoid estate tax Gift to Charity

The Charitable Remainder Trust KEEP SELL CRT E ASSETS$100, 000 EVE$100, 000 RAG L -0 - 20, 000 AVE BEEN -0 ULD H THAT WO APITAL $100, 000 $80, 000 D C $100, 000 TO BUIL TAXED FAMILY R YOUR FO 7% 0 Annual 5% Annual up to 80% ins; Income Annual n capital ga ge o 23% levera Income on pensions) $70, 000 (Up to leverage $40, 000 Estate tax (Double Tax) Income Tax Deduction: $400, 000 Avoid estate tax Gift to Charity

Problem: Donor seeking security is invested in CDs or Bank accounts yielding almost nothing Solution: $100, 000 6% CRT $100, 000 Wurzweiler Endowment! $6, 000 Annual Income $2, 000 Personal Use $2, 000 Annual Wurzweiler Scholarship $2, 000 Insurance

Problem: Donor seeking security is invested in CDs or Bank accounts yielding almost nothing Solution: $100, 000 6% CRT $100, 000 Wurzweiler Endowment! $6, 000 Annual Income $2, 000 Personal Use $2, 000 Annual Wurzweiler Scholarship $2, 000 Insurance

The “Spigot” Trust Have the two life charitable remainder trust purchase insurance on one spouse, or an annuity (net income or nimcrut)

The “Spigot” Trust Have the two life charitable remainder trust purchase insurance on one spouse, or an annuity (net income or nimcrut)

Bad for Charities… Good for You • Charitable gift annuities simply can’t compete with SPIAS, noncharitable indexed, deferred or lifetime annuities • Many charities are somehow reluctant to offer higher yields in charitable trusts • How to sell your annuity while becoming the charity’s friend: • • • Name the charity as successor or contingent beneficiary In lieu of a lower paying charitable gift annuity, contribute cash “spread” from SPIA. INDEXED ANNUITIES/QLACs/LTCI – will all help donor make annual gifts easier.

Bad for Charities… Good for You • Charitable gift annuities simply can’t compete with SPIAS, noncharitable indexed, deferred or lifetime annuities • Many charities are somehow reluctant to offer higher yields in charitable trusts • How to sell your annuity while becoming the charity’s friend: • • • Name the charity as successor or contingent beneficiary In lieu of a lower paying charitable gift annuity, contribute cash “spread” from SPIA. INDEXED ANNUITIES/QLACs/LTCI – will all help donor make annual gifts easier.

The Testamentary Pension Charitable Remainder Trust KEEP $100, 000 -0 - LUMP SUM CRT $100, 000 - 80, 000 ETS -0 E ASS VERAG LE D HAVE $100, 000 T WOUL THA $20, 000 O M$100, 000 AKE XED T EEN TA B MONEY AMILY 7% YOUR F 0 Annual erage) 5% Annual Income 80% Lev Income p to Annual (U Income $1, 000 Estate tax (Double Tax) $7, 000 Income and Possible Estate Tax Deduction: $80, 000 Avoid estate tax Gift to YU

The Testamentary Pension Charitable Remainder Trust KEEP $100, 000 -0 - LUMP SUM CRT $100, 000 - 80, 000 ETS -0 E ASS VERAG LE D HAVE $100, 000 T WOUL THA $20, 000 O M$100, 000 AKE XED T EEN TA B MONEY AMILY 7% YOUR F 0 Annual erage) 5% Annual Income 80% Lev Income p to Annual (U Income $1, 000 Estate tax (Double Tax) $7, 000 Income and Possible Estate Tax Deduction: $80, 000 Avoid estate tax Gift to YU

Donor Opportunities Problems Not For Profit Answers Pensions Bad for Older Donor: Required distributions; High tax money Charitable Pension “salvage” technique gives donor, family, and charity more revenue. Supplemental Pensions Businessman or physician seeks “Supplemental Pension” Charitable Remainder Trust Supplemental Pension (“nimcrut”) Insurance Donor may no longer need or desire paying for insurance. Great vehicle for charities; donor gets tax deduction. Gift of insurance – charity cashes out or sells policy for immediate revenue. Estate Planning: Single donor has federal $5, 430, 000 exemption in 2015 How to transfer assets and values Gift $5, 430, 000 to children with balance to charity; leave high tax pension to charity; consider Lead Trust

Donor Opportunities Problems Not For Profit Answers Pensions Bad for Older Donor: Required distributions; High tax money Charitable Pension “salvage” technique gives donor, family, and charity more revenue. Supplemental Pensions Businessman or physician seeks “Supplemental Pension” Charitable Remainder Trust Supplemental Pension (“nimcrut”) Insurance Donor may no longer need or desire paying for insurance. Great vehicle for charities; donor gets tax deduction. Gift of insurance – charity cashes out or sells policy for immediate revenue. Estate Planning: Single donor has federal $5, 430, 000 exemption in 2015 How to transfer assets and values Gift $5, 430, 000 to children with balance to charity; leave high tax pension to charity; consider Lead Trust

Marketing Insurance and Trusts to Increase Current Gifts • Accelerate bequest into insurance and current cash and perhaps double gift. • Use a CRT to generate more annual cash to donor AND charity. • Use as a legacy gift to sustain annual gift. • Use as a stretch gift. • Promote “virtual endowments” with cash and insurance. • Lead Trust • Instead of gift annuity, obtain SPIA, giving a part of additional income to charity. • Make children “richer” through insurance, SPIAs, indexed annuities, trusts, “charitable Roth arbitragaes, and “supplemental pensions” so you can give more to charity.

Marketing Insurance and Trusts to Increase Current Gifts • Accelerate bequest into insurance and current cash and perhaps double gift. • Use a CRT to generate more annual cash to donor AND charity. • Use as a legacy gift to sustain annual gift. • Use as a stretch gift. • Promote “virtual endowments” with cash and insurance. • Lead Trust • Instead of gift annuity, obtain SPIA, giving a part of additional income to charity. • Make children “richer” through insurance, SPIAs, indexed annuities, trusts, “charitable Roth arbitragaes, and “supplemental pensions” so you can give more to charity.

") “”I WANT TO BE A BENEFACTOR!” (But I don’t have the money right now) Using Insurance to Develop “Stretch” Gifts • Insurance is a way to allow your donors to “stretch” their gifts to meet their charitable goals. • For example, we were recently presented with a supporter who had gifted/pledged a cumulative $600, 000, but lacked the additional $400, 000 to become a Benefactor. • How Do We Make Him a Benefactor? ?

“”I WANT TO BE A BENEFACTOR!” (But I don’t have the money right now) Using Insurance to Develop “Stretch” Gifts • Insurance is a way to allow your donors to “stretch” their gifts to meet their charitable goals. • For example, we were recently presented with a supporter who had gifted/pledged a cumulative $600, 000, but lacked the additional $400, 000 to become a Benefactor. • How Do We Make Him a Benefactor? ?

A Pledge of Insurance • We enabled him to be recognized as a $1, 000 Benefactor by pledging just $35, 000 in “plus” monies every year. How? – The $35, 000 would be used to purchase a $1, 000 insurance policy for YU. Since the supporter is over 60 years old, he and the Advancement Officer would get credit for the present value of this gift of insurance – approximately $400, 000. • The $35, 000 a year “buys” the donor a “gift” of $400, 000 – and opens the door up for him to be considered a Benefactor.

A Pledge of Insurance • We enabled him to be recognized as a $1, 000 Benefactor by pledging just $35, 000 in “plus” monies every year. How? – The $35, 000 would be used to purchase a $1, 000 insurance policy for YU. Since the supporter is over 60 years old, he and the Advancement Officer would get credit for the present value of this gift of insurance – approximately $400, 000. • The $35, 000 a year “buys” the donor a “gift” of $400, 000 – and opens the door up for him to be considered a Benefactor.

The following circumstances are most favorable to a “stretch” gift: • Potential Benefactors who have contributed over $500, 000; • Scholarship donors who would like to perpetualize their gift with a legacy endowment; • Donors who have established programs they would like to see endowed in perpetuity; • Aspiring leaders or board members who cannot contribute as much as they wish: • “Impact” donors and alums who may enjoy broadened recognition possibilities: • Professionals such as physicians and attorneys having a secure income but limited capital: • Donors with illiquid assets such as real estate.

The following circumstances are most favorable to a “stretch” gift: • Potential Benefactors who have contributed over $500, 000; • Scholarship donors who would like to perpetualize their gift with a legacy endowment; • Donors who have established programs they would like to see endowed in perpetuity; • Aspiring leaders or board members who cannot contribute as much as they wish: • “Impact” donors and alums who may enjoy broadened recognition possibilities: • Professionals such as physicians and attorneys having a secure income but limited capital: • Donors with illiquid assets such as real estate.

How to Give $2, 000 to Children and Charity ~For Almost Nothing~

How to Give $2, 000 to Children and Charity ~For Almost Nothing~

Your Pension - or- Good Money vs. Bad Money ~Why the Best Money When You’re Working, Becomes the Worst Money when you Retire ~

Your Pension - or- Good Money vs. Bad Money ~Why the Best Money When You’re Working, Becomes the Worst Money when you Retire ~

The Zero Plan The Hero Plan

The Zero Plan The Hero Plan

Thank you

Thank you

Misc. Slides

Misc. Slides

The Charitable Lead Trust a/k/a, ~ the Jackie Kennedy Trust ~ Transfer up to $20, 000 to family… and $6, 300, 000 to your Foundation… for No Estate Tax at all.

The Charitable Lead Trust a/k/a, ~ the Jackie Kennedy Trust ~ Transfer up to $20, 000 to family… and $6, 300, 000 to your Foundation… for No Estate Tax at all.

The Jackie Kennedy Estate Plan Jackie $40, 000 Friends • $600, 000 among maids and butlers • Sculpture to Maurice Templesman; artwork to friends • Hammersmith Farm to Step-Brother • $500, 000 for each child of Lee Radziwill $10, 000 John Jr. and Caroline • New York Apartment • Art • Personal effects $10, 00 0 Charitable Lead Trust (residual estate) • Income to Charity • Principal to Grandchildren $20, 000

The Jackie Kennedy Estate Plan Jackie $40, 000 Friends • $600, 000 among maids and butlers • Sculpture to Maurice Templesman; artwork to friends • Hammersmith Farm to Step-Brother • $500, 000 for each child of Lee Radziwill $10, 000 John Jr. and Caroline • New York Apartment • Art • Personal effects $10, 00 0 Charitable Lead Trust (residual estate) • Income to Charity • Principal to Grandchildren $20, 000

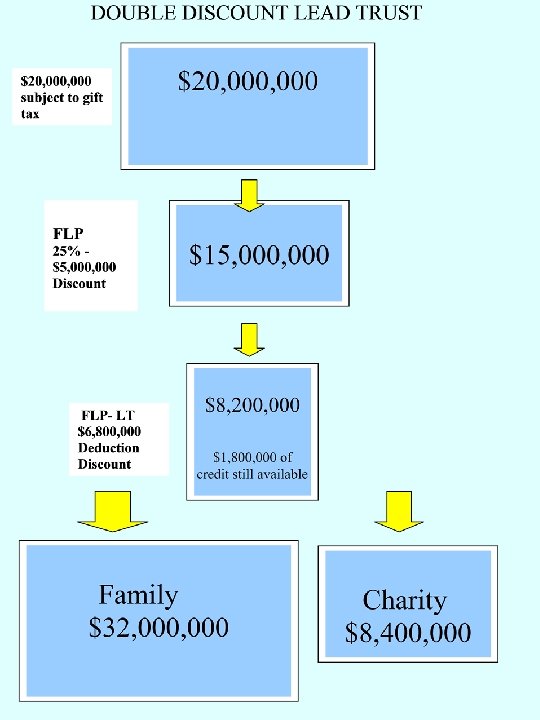

The “Double Discount Lead Trust” The Family Limited Partnership Lead Trust

The “Double Discount Lead Trust” The Family Limited Partnership Lead Trust

~ More Techniques to Build Capital for Family and Charity~ 1. The Leveraged Charitable Remainder Trust • Use CRT to potentially generate 500% more income; invest additional income in strategic insurance to generate potentially 500% more capital! 2. The Lead Trust Income Tax Arbitrage • Use a “defective lead trust” to get a 40% income deduction on money taxed at less than 15% 3. Zero Tax Planning • Move your estate from children and the IRS to children and charity 4. Using Charitable Trusts As Tax Favored “Super Supplemental Retirement Plans”

~ More Techniques to Build Capital for Family and Charity~ 1. The Leveraged Charitable Remainder Trust • Use CRT to potentially generate 500% more income; invest additional income in strategic insurance to generate potentially 500% more capital! 2. The Lead Trust Income Tax Arbitrage • Use a “defective lead trust” to get a 40% income deduction on money taxed at less than 15% 3. Zero Tax Planning • Move your estate from children and the IRS to children and charity 4. Using Charitable Trusts As Tax Favored “Super Supplemental Retirement Plans”