Fixed Assets.pptx

- Количество слайдов: 31

FIXED ASSETS Vahab Hasiri, Arthur Ilgunov, Khristina Terekhina, Viktor Poplavski, Icaro Pazeti

Fixed Assets ■ A fixed asset is a long-term tangible piece of property that a firm owns and uses in the production of its income and is not expected to be consumed or converted into cash any sooner than at least one year's time. Fixed assets are sometimes collectively referred to as "plant. “ ■ Generally, intangible long-term assets such as trademarks and patents are not categorized as fixed assets but are more specifically referred to as fixed intangible assets. ■ A fixed asset is bought for production or supply of goods or services, for rental to third parties, or for use in the organization. Also called property, plant and equipment (PP&E), a fixed asset can include tangible items like laptops and intangible items, such as a copyright, trademark, patent or goodwill. ■ Example: Fixed assets can include buildings, computer equipment, software, furniture, land, machinery and vehicles. For example, if a company sells produce, its delivery trucks are fixed assets. If a business creates a company parking lot, the parking lot is a fixed asset.

Fixed Assets ■ Intangible Goods: An intangible asset is an asset that is not physical in nature. Corporate intellectual property, including items such as patents, trademarks, copyrights and business methodologies, are intangible assets, as are goodwill and brand recognition. ■ Tangible Assets: A tangible asset is an asset that has a physical form. Tangible assets include both fixed assets, such as machinery, buildings and land, and current assets, such as inventory. The opposite of a tangible asset is an intangible asset. ■ Invested Liquid Assets: Investments are considered liquid assets because they can be readily liquidated. For example, shares of stock, bonds, money market funds and mutual funds are considered liquid assets. These assets can be converted to cash in a short period of time in the event a financial emergency arises.

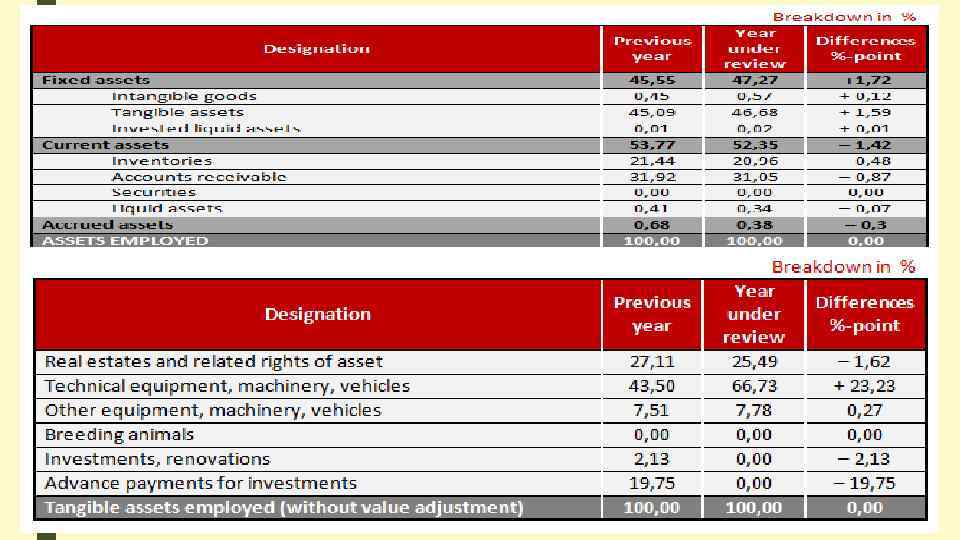

Importance of Fixed Assets ■ Information about a corporation's assets helps create accurate financial reporting, business valuation and thorough financial analysis. Investors use these reports to determine a company's financial health and decide whether to buy shares in or lend money to the business. Because a company may use a range of accepted methods for recording, depreciating and disposing of its assets, analysts need to study the notes on the corporation's financial statements to find out how the numbers were determined.

Evaluation Difference between Evaluation and Valuation: A valuation is performed or placed on an asset to determine its financial worth (or, economic value). "The valuation determined that the car was worth $5, 000. " An evaluation is an analysis of the performance of something or someone, usually against some standard of average performance of similarly situated people or things. "Olga's last work evaluation placed her in the top 5% of her company.

Evaluation The extent to which a project meets intended outputs Relates to how economically activities were undertaken Rigorous analysis of completed or ongoing activities that determine or support management accountability, effectiveness, and efficiency. Fixed Asset: The valuation of property, plant and equipment is performed based on the fixed asset valuation standard that the government/specialists sets the price and calculates the amount of the valuation standard based on that price.

FAIR VALUE The price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date

FAIR VALUE ADJUSTMENT ■ To estimate the price at which an orderly transaction to sell the asset or to transfer the liability would take place between market participants at the measurement date under current market conditions. ■ an entity has to determine all of the following: ü the particular asset or liability that is the subject of the measurement ü for a non-financial asset, the valuation premise that is appropriate for the measurement ü the principal market for the asset or liability ü the valuation technique(s) appropriate for the measurement

FAIR VALUE VALUATION TECHNIQUES ■ MARKET APPROACH ■ COST APPROACH ■ INCOME APPROACH

MARKET APPROACH Market approach uses prices and other relevant information generated by market transactions involving identical or similar assets, liabilities, or a group of assets and liabilities

COST APPROACH Cost approach reflects the amount that would be required currently to replace the service capacity of an asset

INCOME APPROACH Converts future amounts to a single current amount, reflecting current market expectations about those future amounts http: //www. investopedia. com/terms/i/income-approach. asp

Depreciation is an accounting method of allocating the cost of a tangible asset over its useful life. The reason for using: To match a portion of the cost of a fixed asset to the revenue that it generates; this is determined by matching principle, where you record revenues with their associated expenses in the same reporting period in order to give a complete picture of the results of a revenue-generating transaction. Inputs to Depreciation Accounting ü Useful life. This is the time period over which the company expects that the asset will be productive. Depreciation is recognized over the useful life of an asset. ü Salvage value. When a company eventually disposes of an asset, it may be able to sell it for some reduced amount, which is the salvage value. ü Depreciation method.

Straight line method b) Declining")

Depreciation Methods 1. Depreciation methods based on time: a) Straight line method b) Declining balance method c) Sum-of-the-years'-digits method 2. Depreciation based on use (activity):

/ Useful life Example")

Straight Line Depreciation Method Depreciation = (Cost - Residual value) / Useful life Example (Straight line depreciation): On April 1, 2011, Company A purchased an equipment at the cost of $140, 000. This equipment is estimated to have 5 year useful life. At the end of the 5 th year, the salvage value (residual value) will be $20, 000. Company A recognizes depreciation to the nearest whole month. Calculate the depreciation expenses for 2011, 2012 and 2013 using straight line depreciation method. Depreciation for 2011 = ($140, 000 - $20, 000) x 1/5 x 9/12 = $18, 000 Depreciation for 2012 = ($140, 000 - $20, 000) x 1/5 x 12/12 = $24, 000 Depreciation for 2013 = ($140, 000 - $20, 000) x 1/5 x 12/12 = $24, 000

Declining Balance Depreciation Method Depreciation = Book value x Depreciation rate Book value = Cost - Accumulated depreciation Depreciation rate for double declining balance method = Straight line depreciation rate x 200% Depreciation rate for 150% declining balance method = Straight line depreciation rate x 150%

Example of Double declining balance depreciation On April 1, 2011, Company A purchased an equipment at the cost of $140, 000. This equipment is estimated to have 5 year useful life. At the end of the 5 th year, the salvage value (residual value) will be $20, 000. Company A recognizes depreciation to the nearest whole month. Calculate the depreciation expenses for 2011, 2012 and 2013 using double declining balance depreciation method. Useful life = 5 years --> Straight line depreciation rate = 1/5 = 20% per year Depreciation rate for double declining balance method = 20% x 200% = 20% x 2 = 40% per year Depreciation for 2011 = $140, 000 x 40% x 9/12 = $42, 000 Depreciation for 2012 = ($140, 000 - $42, 000) x 40% x 12/12 = $39, 200 Depreciation for 2013 = ($140, 000 - $42, 000 - $39, 200) x 40% x 12/12 = $23, 520

Double Declining Balance Depreciation Method Year Book Value at the beginning Depreciation Rate 40% Depreciation Expense $42, 000 (*1) Book Value at the year-end 2011 $140, 000 $98, 000 2012 $98, 000 40% $39, 200 (*2) $58, 800 2013 $58, 800 40% $23, 520 (*3) $35, 280 2014 $35, 280 40% $14, 112 (*4) $21, 168 2015 $21, 168 40% $1, 168 (*5) $20, 000 (*1) $140, 000 x 40% x 9/12 = $42, 000 (*2) $98, 000 x 40% x 12/12 = $39, 200 (*3) $58, 800 x 40% x 12/12 = $23, 520 (*4) $35, 280 x 40% x 12/12 = $14, 112 (*5) $21, 168 x 40% x 12/12 = $8, 467 --> Depreciation for 2015 is $1, 168 to keep book value same as salvage value. --> $21, 168 - $20, 000 = $1, 168 (At this point, depreciation stops. )

x")

Sum of the years‘ digits method Depreciation expense = (Cost - Salvage value) x Fraction for the first year = n / (1+2+3+. . . + n) Fraction for the second year = (n-1) / (1+2+3+. . . + n) Fraction for the third year = (n-2) / (1+2+3+. . . + n). . . Fraction for the last year = 1 / (1+2+3+. . . + n) n represents the number of years for useful life.

Example Of Sum-of-the-years-digits method Company A purchased the following asset on January 1, 2011. What is the amount of depreciation expense for the year ended December 31, 2011? Acquisition cost of the asset --> $100, 000 , Useful life of the asset --> 5 years Residual value (or salvage value) at the end of useful life --> $10, 000 Depreciation method --> sum-of-the-years'-digits method Calculation of depreciation expense: Sum of the years' digits = 1+2+3+4+5 = 15 Depreciation for 2011 = ($100, 000 - $10, 000) x 5/15 = $30, 000 Depreciation for 2012 = ($100, 000 - $10, 000) x 4/15 = $24, 000 Depreciation for 2013 = ($100, 000 - $10, 000) x 3/15 = $18, 000 Depreciation for 2014 = ($100, 000 - $10, 000) x 2/15 = $12, 000 Depreciation for 2015 = ($100, 000 - $10, 000) x 1/15 = $6, 000 Sum of the years' digits for n years= 1 + 2 + 3 +. . . + (n-1) + n = (n+1) x (n / 2) Sum of the years' digits for 500 years= 1 + 2 + 3 +. . . + 499 + 500 = (500 + 1) x (500 / 2) = (501 x 500) / 2 = 125, 250

The activity method of depreciation (also called the variable")

Depreciation based on use (activity) The activity method of depreciation (also called the variable charge approach) assumes that depreciation is a function of use or productivity instead of the passage of time. The life of the asset is considered in terms of either the output it provides (units of produces), or an input measure such as the number of hours it works. Conceptually, the proper cost association is established in terms of output instead of hours used, but often the output is not easily measurable. In such cases, an output measure such as machine hours is a more appropriate method of measuring the dollar amount of depreciation charges for a given accounting period. The following formula is used for the calculation of depreciation charge under activity method: (Cost less salvage value) × Hours this year / Total estimated hours = Depreciation charge

Example Assume that a company purchased a crane for digging purposes. Pertinently data concerning the purchase of the crane are: Cost of crane $500, 000 Estimated useful life 5 years Estimated salvage value $50, 000 Productive life in hours 30, 000 hours If the crane is used 4, 000 hours the first year, the depreciation charge is: (Cost less salvage value) × Hours this year/Total estimated hours = Depreciation Charge ($500, 000 - $50, 000) × 4, 000/30, 000 = $60, 000

Who Uses Activity Method of Depreciation: Where losses of services is a result of activity or productivity, the activity method will best match costs with revenues. Companies that desire low depreciation during periods of low productivity and high depreciation during high productivity either adopt or switch to an activity method of depreciation. In this way plant running at 40 percent of capacity generates 60 percent lower depreciation charges. Real Business Example Inland Steel switched to units of production depreciation (variable charge approach) at one time and reduced its losses by $43 million or $1. 20 per share

Limitations of Activity Method of Depreciation: ■ The major limitation of activity method is that it is not appropriate in situations in which depreciation is a function of time instead of activity. For example, a building is subject to a great deal of steady deterioration from the elements (time) regardless of its use. In addition, where an asset is subject to economic or functional factors, independent of its use, the activity method loses much of its significance. For example, if a company is expanding rapidly, a particular building may soon become obsolete for its intended purposes. In both cases activity is irrelevant. Another problem in using this method is that an estimate of units of output or service hours received is often difficult to determine.

Impairment recognition ■ Asset badly damaged ■ Asset´s market price has been significantly reduced ■ Legal issues have had a negative impact on the asset ■ Asset is set for disposal before the end of its useful life

Indications of impairment External sources Internal sources ■ obsolescence or physical damage ■ market value declines ■ negative changes in technology, markets, economy, or laws ■ asset is idle, part of a restructuring or held for disposal ■ worse economic performance than expected ■ increases in market interest rates ■ net assets of the company higher than market capitalization ■ for investments in subsidiaries, joint ventures or associates, the carrying amount is higher than the carrying amount of the investee's assets, or a dividend exceeds the total comprehensive income of the investee

: USD 20. 000 ■")

Example ■ Non-current worth (recorded on the balance sheet) : USD 20. 000 ■ Historical cost : USD 25. 000 and accumulated depreciation USD 5. 000 ■ Stores building was damaged after a hurricane –> fallen market value to USD 12. 000 – Debit loss on Impairment = USD 8. 000 (20. 000 book value – 12. 000 market value) – Debit store building-accumulated depreciation = USD 5. 000 – Credit store building = USD 13. 000

Disposal of assets ■ If a company disposes of a long-term asset for an amount different from its recorded amount in the company's accounting records, an adjustment must be made to net income on the cash flow statement.

Disposal of assets: example ■ Truck original costs : USD 20. 000 – Accumulated depreciation : USD 18. 000 – book value USD 2. 000 (20. 000 – 18. 000) – Proceeds from sale : USD 3. 000 ■ USD 1. 000 recorded in the account Gain on Sal of Truck

Thank you for your attention

Fixed Assets.pptx